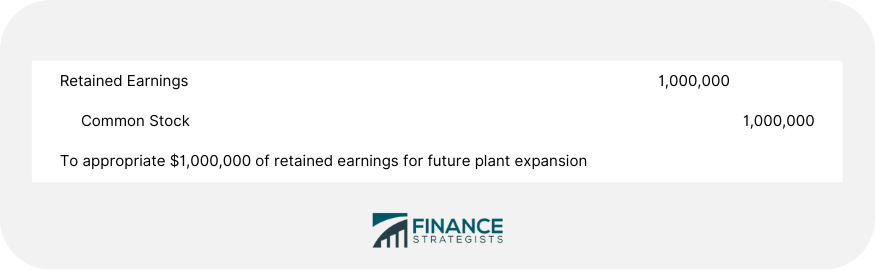

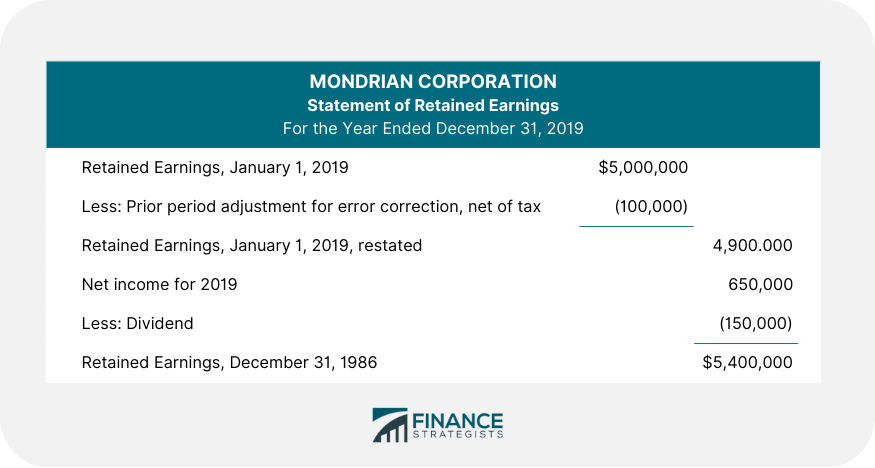

Prior period adjustments are the transactions that relate to an earlier accounting period but that were not determinable by management in the earlier period. Under the all-inclusive concept of income, with a few exceptions, all items of profit and loss recognized during the period are included in net income for the period. These exceptions mainly relate to prior period adjustments and are accounted for by an adjustment to the beginning balance of retained earnings. There has been, however, considerable controversy about what causes an event to qualify as a prior period adjustment. Only two events are considered prior period adjustments: Because the realization of tax benefits is a specialized topic, we will examine only prior adjustments that relate to error corrections. Occasionally, a firm will discover a material error in a prior year’s financial statements. However, material errors are very rare, especially when a firm’s financial statements are audited by a CPA firm. When they do occur and are discovered, the manner in which the error is corrected depends on whether the firm publishes single-year or comparative financial statements and on the year in which the error was made. When single-year statements are published, the error is corrected by adjusting the beginning balance of retained earnings on the retained earnings statement. To demonstrate accounting for prior period adjustments in a single-year statement, we will assume that during the audit of its 2019 statements, the Mondrian Corporation discovered that depreciation in 2018 had been understated by $100,000, ignoring taxes. Because this is a material error, a prior period adjustment is required. The following journal entry is made at year-end to correct this error: The 2019 statement of retained earnings would appear as follows: In addition, the prior period adjustment is explained in the footnotes to the financial statement. When comparative financial statements are presented, the procedure is different. If the error is in an earlier financial statement that is being presented for comparative purposes, that statement should be revised to correct the error. As a result, net income will be corrected, and after that corrected net income figure is reflected on the retained earnings statement, no further adjustment is required. If the error is in a year for which the financial statements are not being presented, the correction is made through a prior period adjustment to the earliest retained earnings balance presented.Explanation

Example

Prior Period Adjustments FAQs

A prior period adjustment is used to adjust financial statements from a previous accounting period to reflect changes or corrections that were not recorded in the original accounting period. This helps ensure that all financial information is reported accurately and consistently over time.

Prior period adjustments are typically classified as either correcting adjustments or non-correcting adjustments, depending on the type of change being made. Correcting adjustments include changes related to errors or misstatements from prior periods, while non-correcting adjustments are typically related to new information or changes in estimates for existing transactions.

Generally, the responsibility of determining if an adjustment is necessary falls to management or external auditors. They will review the financial statements and determine if any changes need to be made that were not reflected in the original accounting period.

Prior period adjustments can either increase or decrease net income depending on the type of adjustment being made. Correcting adjustments typically result in a decrease in net income, while non-correcting adjustments usually increase net income.

Examples of correcting prior period adjustments include changes related to errors or misstatements from past accounting periods, such as misclassifying an expense as a revenue item. Examples of non-correcting prior period adjustments include changes related to new information or changes in estimates for existing transactions, such as revising the estimated useful life of a fixed asset.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.