A Roth IRA is an individual retirement account funded with after-tax dollars. That means you generally do not deduct Roth IRA contributions the way you may deduct some traditional IRA contributions. The trade-off is that qualified Roth IRA withdrawals can be tax-free. That creates a common misunderstanding. Many people assume that because Roth IRAs are funded with after-tax money, there are no tax forms involved. Not quite. A Roth IRA is still a tax-advantaged retirement account, and certain activity is reported to the IRS. Roth IRAs are built around three basic tax ideas. First, contributions are generally made with pre-tax income. You usually do not get an upfront tax deduction. Second, investments inside the Roth IRA can grow tax-deferred and potentially tax-free. If your Roth IRA owns stocks, mutual funds, ETFs, or bonds, the account itself generally does not send you taxable dividend or capital gain forms each year the way a regular brokerage account might. Third, withdrawals may be tax-free if they meet the qualified distribution rules. IRS Publication 590-B explains the rules for IRA distributions, including when distributions may be taxable and when penalties may apply. You may get tax forms for your Roth IRA. But the form depends on the activity. If you contributed to a Roth IRA, your custodian may send Form 5498. If you took money out, you may receive Form 1099-R. If you completed a Roth conversion, you may receive both forms because money left one retirement account and entered a Roth IRA. If you only held investments in the Roth IRA and made no contributions, withdrawals, conversions, rollovers, or corrections, you may not receive a Roth IRA tax form for that year. Form 5498 is the form that reports IRA contributions and certain IRA account activity. For Roth IRAs, this can include regular Roth IRA contributions, rollover contributions, and Roth conversion amounts. This form is usually sent by the IRA trustee, custodian, or issuer. It is also sent to the IRS. The taxpayer keeps it for records. Form 5498 matters because Roth IRA contribution history can become important later. If you withdraw money from a Roth IRA before the account is fully qualified, your records can help show how much of the account came from contributions, conversions, and earnings. Form 1099-R reports distributions from retirement accounts, including IRAs. The IRS says Form 1099-R applies when someone receives, or is treated as having received, a distribution of $10 or more from an IRA or certain other retirement arrangements. For a Roth IRA, this can include withdrawals, rollovers, conversions, inherited Roth IRA distributions, and certain corrective distributions. A Form 1099-R does not automatically mean the entire amount is taxable. It means money came out of the account and the transaction needs to be reported. A Roth IRA tax form is not the same thing as a tax bill. Form 5498 is often informational. Form 1099-R reports a distribution, but the tax result depends on the type of money withdrawn and whether the distribution qualifies for tax-free treatment. For example, a Roth IRA withdrawal may include original contributions, converted amounts, or earnings. Those categories can be treated differently. A qualified distribution may be tax-free. A non-qualified withdrawal of earnings may be taxable and may also be subject to an additional penalty. If the only thing you did was contribute to your Roth IRA, Form 5498 is usually the form to know. It is not usually a form that directly changes your tax return. But it is still worth keeping. Roth IRA contributions are generally reported on Form 5498. The form helps the IRS track IRA contributions and related account activity. This does not mean your Roth IRA contribution is deductible. Roth IRA contributions are typically made with after-tax dollars. Unlike some traditional IRA contributions, a regular Roth IRA contribution usually does not reduce taxable income. Still, the IRS wants a record of the contribution. That record can matter for contribution limits, eligibility rules, and future withdrawal treatment. You generally do not attach Form 5498 to your tax return. This is one of the most important points for readers. Many people receive the form and assume they need to amend a return or send the form somewhere. Usually, no. Form 5498 is typically for recordkeeping. The custodian sends it to the IRS, and you keep your copy with your tax documents. If your contribution amount is correct and there are no eligibility issues, the form may not require any action. Form 5498 often arrives after the regular tax filing deadline. The timing makes sense because IRA contributions for a tax year can often be made until the tax filing deadline of the following year. A custodian may need to wait until that window closes before finalizing contribution reporting. So if you receive Form 5498 after you already filed your tax return, that is not automatically a problem. In many cases, it is normal. Roth IRA records can matter years later, especially if you take a non-qualified distribution. Your contribution history helps show how much money you have already paid tax on. That matters because Roth IRA contributions can often be withdrawn more favorably than earnings. If you cannot document your contribution history, figuring out the taxable portion of a future withdrawal may become harder. Form 1099-R is more likely to affect your tax return than Form 5498. If you took money out of a Roth IRA, received an inherited Roth IRA distribution, corrected an excess contribution, or converted funds from another retirement account, this form deserves careful attention. A Roth IRA withdrawal is generally reported on Form 1099-R. The form shows the gross distribution, any taxable amount known to the custodian, federal income tax withheld, and a distribution code. The distribution code matters because it gives information about the type of distribution. However, custodians may not always know your full tax situation. They may not know your entire Roth IRA contribution history, five-year rule status, or whether you qualify for an exception. That means the taxpayer may need to determine the final taxable amount. A Roth IRA withdrawal can be tax-free, partially taxable, or taxable. The answer depends on what came out of the account. Original Roth IRA contributions are generally treated more favorably because they were made with after-tax dollars. Earnings are different. If earnings are withdrawn before the distribution is qualified, they may be taxable. Converted amounts can also require special attention. A conversion may have its own timing rules, and early access to converted funds can create unexpected tax or penalty issues. A qualified Roth IRA distribution is generally the cleanest outcome. To be qualified, a Roth IRA distribution typically must satisfy the applicable five-year holding period and meet another condition, such as being made after age 59½, because of disability, after death, or for certain first-time homebuyer purposes. Publication 590-B discusses Roth IRA distributions and the rules that determine whether they are taxable. When a distribution is qualified, the earnings portion can generally come out tax-free. This is another common point of confusion. If you withdraw only your regular Roth IRA contributions, the withdrawal may not be taxable because those contributions were already taxed. The problem usually arises when the withdrawal reaches earnings or certain converted amounts. For example, someone who contributed $20,000 over time and has a Roth IRA worth $28,000 may assume every dollar is treated the same. It is not. The original contribution layer and the earnings layer can have different tax consequences. Form 1099-R may also show federal income tax withheld. Withholding is not the same as tax owed. It is a prepayment. If too much was withheld, it could increase your refund. If too little was withheld and the distribution was taxable, you may owe additional tax when you file. A Roth conversion happens when money from a pre-tax retirement account, such as a traditional IRA, is moved into a Roth IRA. This usually creates tax reporting. The distributing account may issue Form 1099-R. The receiving Roth IRA may issue Form 5498 showing the conversion contribution. A Roth conversion can also create taxable income. If the converted money was pre-tax, the conversion generally brings that amount into taxable income for the year. This is one reason Roth conversions should be planned carefully. Rollovers may also generate tax forms. For example, if someone moves money from a Roth 401(k) to a Roth IRA, the transaction may be reported even if it is not taxable when handled correctly. The source account may issue Form 1099-R, and the receiving Roth IRA may report the rollover on Form 5498. The key issues are whether the rollover was direct or indirect, whether it was properly completed, and whether the money was pre-tax or after-tax. A trustee-to-trustee transfer is often cleaner than an indirect rollover because the money moves directly between institutions. Still, taxpayers should not assume every transfer is invisible. The reporting depends on the type of account, the type of transfer, and how the custodian classifies the transaction. When in doubt, review the tax form, distribution code, and account statement. A conversion may increase taxable income in the year of conversion. That can affect tax brackets, credits, deductions, health insurance subsidies, student aid calculations, or Medicare-related thresholds for some taxpayers. The benefit is that future qualified Roth IRA withdrawals may be tax-free. The cost is often the tax bill today. An excess Roth IRA contribution can happen for several reasons. A taxpayer may contribute more than the annual limit. A high-income taxpayer may contribute directly to a Roth IRA even though their income is above the allowed range. Someone may contribute without sufficient earned income. These mistakes are common because Roth IRA eligibility depends on income, filing status, compensation, and annual contribution limits. Correcting an excess Roth IRA contribution may generate Form 1099-R. If the excess amount is removed, the custodian may report the corrective distribution. If earnings are also removed, those earnings may have their own tax treatment. The timing matters. Correcting the issue before the deadline can produce a different result than leaving the excess contribution in the account. Earnings connected to an excess contribution can be taxable depending on the facts. This is where the issue becomes more than clerical. The excess contribution itself may have been made with after-tax money, but the earnings related to that excess contribution may need to be reported. Because excess contribution rules can become technical quickly, this is one area where professional tax guidance may be worth the cost. You may not receive a Roth IRA tax form if there was no reportable activity during the year. For example, if you already had a Roth IRA and simply left the investments alone, there may be no Form 5498 or Form 1099-R to send. Investment growth inside the account does not usually create annual taxable income reporting. You may also not receive a form if the amount or activity does not meet the reporting threshold, or if the form is only available electronically through your custodian’s website. Most custodians provide tax forms in an online document center. Look for a section labeled “Tax Forms,” “Statements and Documents,” or “Tax Documents.” Forms may be posted before paper copies arrive. If you elected electronic delivery, you may not receive anything by mail. For Form 1099-R, check early in tax season. For Form 5498, expect later availability in many cases. If a Roth IRA tax form looks wrong, contact the custodian. Common issues include incorrect contribution amounts, unexpected distribution codes, missing rollover treatment, or a taxable amount that does not match your records. Do not ignore a form just because you believe it is wrong. The IRS may also receive a copy. Custodians can issue corrected tax forms. If a mistake is confirmed, ask whether a corrected Form 1099-R or Form 5498 will be issued. If you already filed your tax return using incorrect information, you may need to ask a tax professional whether an amended return is necessary. A Roth IRA contribution is generally made with after-tax dollars and is not deductible. A traditional IRA contribution may be deductible, depending on income, filing status, and workplace retirement plan coverage. That difference changes how the contribution affects the tax return. Both accounts may involve Form 5498, but the tax results are different. Traditional IRA withdrawals are often taxable because many traditional IRA contributions were made pre-tax or deducted. Roth IRA withdrawals may be tax-free if they meet the qualified distribution rules. Even nonqualified Roth IRA withdrawals may include contribution amounts that are not taxable. That is why Form 1099-R must be read in context. The same form can report very different tax outcomes. Form 5498 and Form 1099-R are reporting forms. They do not tell the whole tax story by themselves. For a traditional IRA, a distribution may often be taxable. For a Roth IRA, the distribution may be tax-free, partially taxable, or taxable depending on the withdrawal source and timing. The form is the starting point. The tax rules determine the result. Many taxpayers do not need to wait for Form 5498 before filing their tax return. Since Form 5498 often arrives after the filing deadline, waiting for it can create unnecessary delay. If you know your contribution amount and are eligible to contribute, the form is usually just a confirmation for your records. A Form 1099-R means a distribution was reported. It does not automatically mean the distribution is taxable. This is especially important for Roth IRAs. A withdrawal of contributions may be tax-free. A qualified distribution may be tax-free. The key is determining what portion, if any, is taxable. Form 5498 may not feel important when it arrives, but it can matter later. It helps document your Roth IRA contributions, conversions, and rollovers. That history can support your position if you later take withdrawals and need to show how much of the account represents already-taxed money. A Roth IRA contribution can create problems if the taxpayer was not eligible to make it. Income limits, filing status, contribution limits, and compensation requirements all matter. If a contribution is excessive or ineligible, it may need to be corrected. The Roth IRA five-year rule can affect whether earnings are tax-free. This is especially important for newer Roth IRAs, conversions, and early withdrawals. A taxpayer may be over age 59½ but still need to consider whether the five-year requirement has been met for qualified distribution purposes. You may get tax forms for your Roth IRA, but it depends on your account activity. If you contributed to a Roth IRA, you may receive Form 5498. If you withdrew money, completed a conversion, rolled funds over, inherited a Roth IRA distribution, or corrected an excess contribution, you may receive Form 1099-R. Form 5498 is usually for your records. Form 1099-R is more likely to affect your tax return, although it does not automatically mean you owe tax. The best approach is simple: review every Roth IRA tax form, keep good records, and pay special attention to withdrawals, conversions, and excess contributions. Roth IRAs can be tax-friendly, but they are not tax-form-free. For more information and expert guidance, consult a tax attorney or financial advisor.Roth IRA: Overview

How Roth IRAs Are Taxed

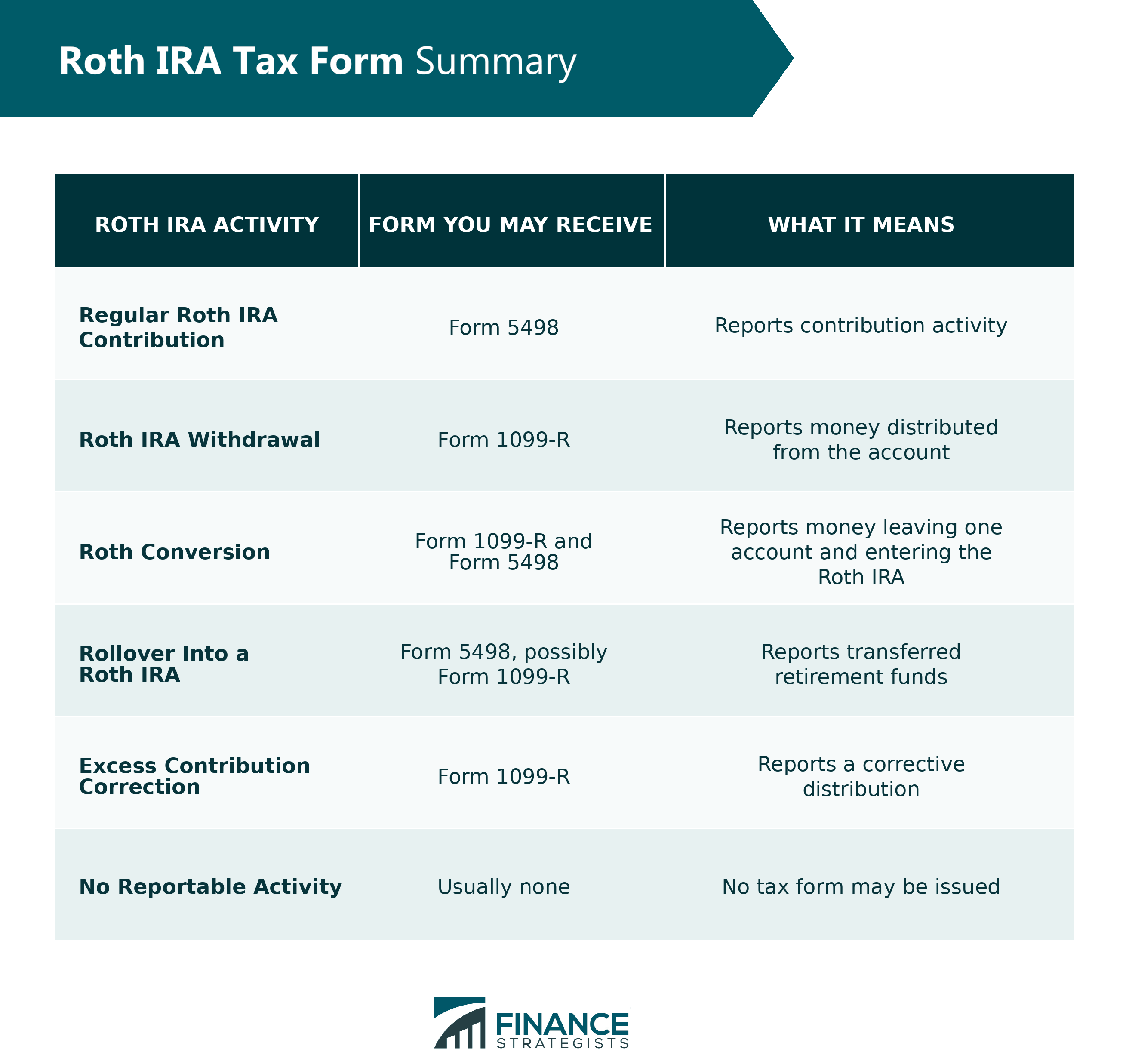

Do You Get Tax Forms for Your Roth IRA?

Roth IRA Tax Forms You May Receive

Form 5498 for Roth IRA Contributions

Form 1099-R for Roth IRA Distributions

Why a Tax Form Does Not Always Mean You Owe Tax

Form 5498 and Roth IRA Contributions

Contribution Reporting

Filing Requirements

Late Arrival After Tax Day

Recordkeeping for Roth IRA Basis

Form 1099-R and Roth IRA Withdrawals

Distribution Reporting

Taxable Versus Tax-Free Withdrawals

Qualified Roth IRA Distributions

Early Roth IRA Withdrawals

Federal Tax Withholding

Roth Conversions, Rollovers, and Transfers

Roth Conversions

Rollovers Into a Roth IRA

Trustee-to-Trustee Transfers

Taxable Income From Roth Conversions

Excess and Corrective Distributions

Excess Roth IRA Contributions

Correcting an Excess Contribution

Earnings on Excess Contributions

Missing, Delayed, or Incorrect Roth IRA Tax Forms

Reasons You May Not Receive a Form

Where to Find Your Roth IRA Tax Forms

Incorrect Roth IRA Tax Forms

Corrected Tax Forms

Roth vs Traditional IRA Tax Forms

Contribution Differences

Distribution Differences

Why the Same Forms Can Mean Different Things

Roth IRA Tax Form Mistakes to Avoid

Waiting for Form 5498 Before Filing

Assuming Form 1099-R Means You Owe Tax

Throwing Away Form 5498

Ignoring Roth IRA Income and Contribution Limits

Forgetting About the Five-Year Rule

Bottom Line

Do You Get Tax Forms for Your Roth IRA? FAQs

Yes. Roth IRA contributions are generally reported on Form 5498. The form is usually sent by the IRA custodian and is also reported to the IRS.

Usually, no. Form 5498 is generally for your records. It often arrives after the tax filing deadline, so many taxpayers file before receiving it.

Not always. A Roth IRA 1099-R reports a distribution, but the taxability depends on whether the withdrawal was qualified, whether it included earnings, and whether any exceptions apply.

Usually, dividends earned inside a Roth IRA do not generate annual taxable dividend forms for the account owner. The investments grow inside the tax-advantaged account, so the reporting is different from a regular taxable brokerage account.

Contact the IRA custodian and ask for clarification. If the form is incorrect, ask whether a corrected form will be issued. Do not ignore the form, because the IRS may have received the same information.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.