Actuarial gain or loss refers to the difference between expected and actual pension plan experience. Specifically, it is the difference between the projected benefit obligation (PBO) and the fair value of plan assets at the end of a period. Actuarial gains or losses are an important consideration for pension plan sponsors and can have a significant impact on plan funding, expense recognition, and financial statements. Actuarial gain or loss is a critical concept for pension plan sponsors to understand, as it can have a significant impact on the financial health of the plan and the sponsor's financial statements. By understanding the factors that contribute to actuarial gain or loss and the methods for calculating it, plan sponsors can take steps to manage this risk and ensure that their plans remain sustainable over the long term. Actuarial gain occurs when the actual experience of the pension plan exceeds the assumptions that were used to calculate the PBO. This can occur when actual employee turnover is lower than expected, when actual mortality rates are lower than expected, or when actual salary growth is lower than expected. When actuarial gain occurs, the fair value of plan assets will be less than the PBO, resulting in a gain for the plan sponsor. Actuarial loss occurs when the actual experience of the pension plan falls short of the assumptions that were used to calculate the PBO. This can occur when actual employee turnover is higher than expected, when actual mortality rates are higher than expected, or when actual salary growth is higher than expected. When actuarial loss occurs, the fair value of plan assets will be greater than the PBO, resulting in a loss for the plan sponsor. For example, if a pension plan assumes that employees will retire at an average age of 65, but in reality, many employees retire earlier, the plan may experience an actuarial gain. Similarly, if the plan assumes that employees will live to an average age of 85, but in reality, many employees live longer, the plan may experience an actuarial loss. Changes in assumptions, such as changes in interest rates, mortality rates, or salary growth rates, can have a significant impact on actuarial gain or loss. If actual experience is different from the assumptions used to calculate the PBO, actuarial gain or loss may result. Experience gains or losses refer to the difference between the actual experience of the plan and the assumptions used to calculate the PBO. For example, if employee turnover is lower than expected, the plan may experience an experience gain, as the plan will have fewer retirees than expected. Demographic changes, such as changes in the age or gender distribution of plan participants, can also impact actuarial gain or loss. For example, if a plan has a higher than expected number of female retirees, the plan may experience an actuarial loss, as females tend to live longer than males on average. Finally, differences between the expected and actual return on plan assets can also contribute to actuarial gain or loss. If the plan earns a higher than expected return on its investments, the plan may experience an actuarial gain, as the fair value of plan assets will be higher than expected. The projected unit credit method is a common method for calculating actuarial gain or loss. This method calculates the PBO by taking into account the employee's expected future compensation, as well as the expected number of years until retirement and life expectancy. Actuarial gain or loss is then calculated based on any differences between actual and expected experience. The entry age normal method is another method for calculating actuarial gain or loss. This method assumes that all employees will retire at a predetermined age, such as age 65. Actuarial gain or loss is then calculated based on any differences between actual and expected experience, using this assumption. The attained age method is a simpler method for calculating actuarial gain or loss. This method assumes that all employees will retire at their current age. Actuarial gain or loss is then calculated based on any differences between actual and expected experience, using this assumption. Actuarial gain or loss can have a significant impact on pension plan funding. If the plan experiences an actuarial gain, the plan sponsor may be able to reduce contributions to the plan, as the fair value of plan assets will be greater than expected. On the other hand, if the plan experiences an actuarial loss, the plan sponsor may be required to make additional contributions to the plan to ensure that it remains fully funded. Actuarial gain or loss can also impact pension plan expense recognition. For example, if a plan experiences an actuarial gain, the plan sponsor may recognize a reduction in pension expense, as the expected benefit obligation will be lower than expected. Conversely, if a plan experiences an actuarial loss, the plan sponsor may recognize an increase in pension expense, as the expected benefit obligation will be higher than expected. Finally, actuarial gain or loss can impact the financial statements of the plan sponsor. If the plan sponsor recognizes an actuarial gain, the fair value of plan assets will be greater than the PBO, resulting in a gain for the sponsor. Conversely, if the plan sponsor recognizes an actuarial loss, the fair value of plan assets will be less than the PBO, resulting in a loss for the sponsor. One way to manage actuarial gain or loss is through risk management strategies, such as hedging or diversification. By implementing these strategies, plan sponsors can help to minimize the impact of market volatility on plan assets, reducing the risk of significant actuarial gain or loss. Investment management strategies can also help to manage actuarial gain or loss. By investing in a diversified portfolio of assets that is designed to generate consistent returns over the long term, plan sponsors can reduce the risk of significant fluctuations in the fair value of plan assets. Finally, actuarial assumptions and methods can also be adjusted to help manage actuarial gain or loss. By using conservative assumptions and methods, plan sponsors can help to minimize the risk of significant actuarial gain or loss, ensuring that their plans remain sustainable over the long term. Actuarial gain or loss is a critical concept for pension plan sponsors to understand, as it can have a significant impact on plan funding, expense recognition, and financial statements. By understanding the factors that contribute to actuarial gain or loss, and the methods for calculating it, plan sponsors can take steps to manage this risk and ensure that their plans remain sustainable over the long term. By implementing effective risk management and investment management strategies, and by using conservative actuarial assumptions and methods, plan sponsors can help to minimize the risk of significant actuarial gain or loss, and ensure the long-term financial health of their pension plans. Additionally, plan sponsors may also want to consider working with a qualified actuary to help manage this risk and ensure compliance with applicable regulations and accounting standards. Overall, actuarial gain or loss is a complex concept that requires a thorough understanding of pension plan mechanics, actuarial assumptions and methods, and financial management strategies. By taking the time to fully understand this concept and its implications for their pension plans, plan sponsors can help to ensure the financial health and sustainability of their plans over the long term.What Is Actuarial Gain or Loss?

Explaining Actuarial Gain or Loss

Explanation of Actuarial Gain

Explanation of Actuarial Loss

Examples of Actuarial Gain and Loss

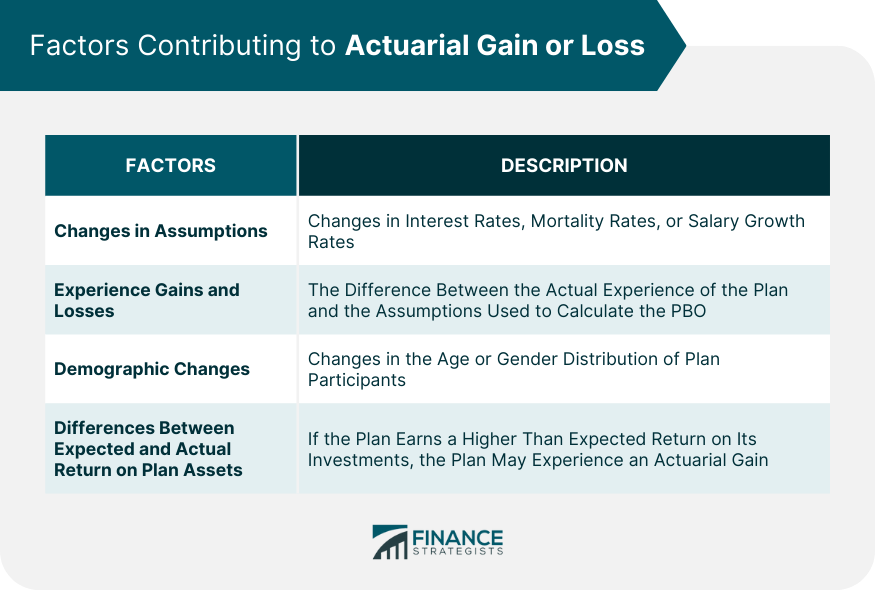

Factors Contributing to Actuarial Gain or Loss

Changes in Assumptions

Experience Gains and Losses

Demographic Changes

Differences Between Expected and Actual Return on Plan Assets

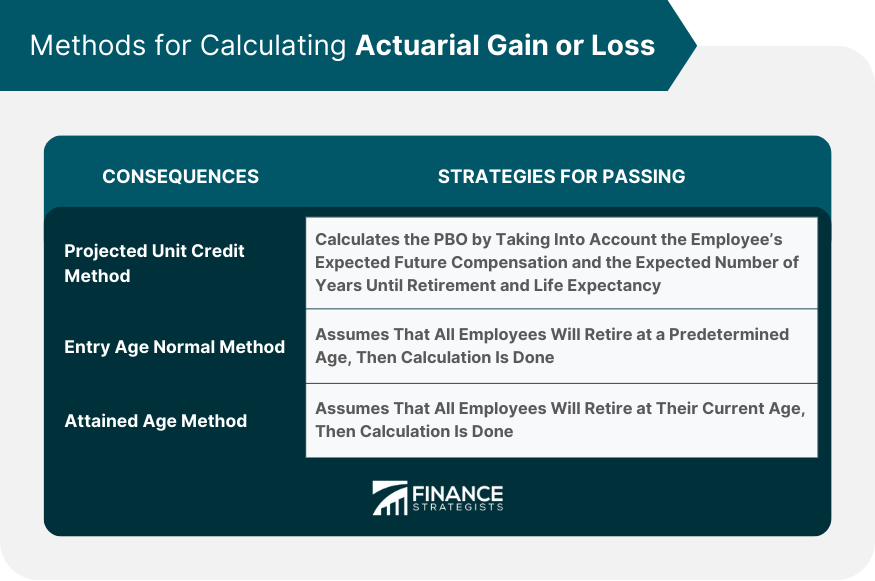

Methods for Calculating Actuarial Gain or Loss

Projected Unit Credit Method

Entry Age Normal Method

Attained Age Method

Impact of Actuarial Gain or Loss

Impact on Pension Plan Funding

Impact on Pension Plan Expense Recognition

Impact on Financial Statements

Managing Actuarial Gain or Loss

Risk Management Strategies

Investment Management Strategies

Actuarial Assumptions and Methods

Conclusion

Actuarial Gain or Loss FAQs

Actuarial gain or loss is the difference between expected and actual experience in pension plans, including changes in assumptions and investment returns.

Actuarial gain or loss is typically calculated using actuarial methods, such as the projected unit credit method, entry age normal method, or attained age method.

Actuarial gain or loss can have significant impact on pension plan funding, expense recognition, and financial statements.

Actuarial gain or loss can be managed through risk management strategies, investment management strategies, and careful selection of actuarial assumptions and methods.

Actuarial gain or loss is important because it can affect the financial stability of pension plans, as well as the financial statements and performance of the organizations that sponsor them.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.