A retirement plan termination refers to the process of ending a retirement plan, either voluntarily or involuntarily, which includes the distribution of all remaining plan assets to participants and beneficiaries. Termination may result from a variety of factors, including financial hardship, company restructuring, or changes in company strategy. Understanding the retirement plan termination process is crucial for both employers and employees, as it can impact future financial planning, retirement security, and tax implications. Being aware of the process can help all parties involved to navigate it more effectively and ensure a smooth transition. Several factors can influence a company's decision to terminate a retirement plan, including economic circumstances, business objectives, regulatory compliance issues, or changes in the workforce. By assessing these factors, employers can make informed decisions about whether plan termination is the best course of action. Defined benefit plans are employer-sponsored retirement plans that provide a predetermined, fixed benefit upon retirement, usually based on factors like years of service and salary history. These plans are less common today, as they place more financial risk on the employer due to the guarantee of a specific retirement income. Defined contribution plans, on the other hand, allow employees and employers to contribute a predetermined amount to an individual account. Defined contribution plans shift investment risk from employer to employee, with retirement benefits based on investment performance. Popular 401(k) plans offer tax-deferred investment growth and employer contribution matching. IRAs offer personal retirement savings with tax advantages while profit-sharing plans allocate a portion of company profits to employee retirement accounts. ESOPs enable partial employee ownership of company stock, fostering a sense of responsibility and alignment with the company's success. One reason for retirement plan termination may be company restructuring or bankruptcy, where an organization may need to liquidate assets or reorganize its operations to remain viable. In such cases, terminating a retirement plan might be necessary to free up resources or simplify the business structure. Another reason for plan termination is the merger or acquisition of companies. When two organizations combine, their retirement plans may also need to be merged, resulting in the termination of one or both plans in order to create a new, unified retirement plan for the combined workforce. Retirement plan termination can also be triggered by plan underperformance or mismanagement, where the plan's investments are not performing well or the plan is not being managed effectively. In these cases, employers may choose to terminate the plan to protect participants' interests and find a more suitable retirement savings option. Retirement plans must adhere to strict regulations, and failure to comply with these rules can result in plan termination. This may occur due to a company's inability to meet funding requirements, nondiscrimination rules, or other regulatory guidelines. Termination may be necessary to address these compliance issues and avoid potential penalties. A change in company strategy or objectives can also lead to retirement plan termination. For example, a company might shift its focus to attracting younger talent, leading to the discontinuation of a traditional defined benefit plan in favor of a more flexible defined contribution plan, better suited to the evolving workforce. The first step in the retirement plan termination process is notifying plan participants of the impending termination. Employers are required to provide written notice to all participants, informing them of the termination, the reasons behind it, and the expected timeline for the distribution of plan assets. Plan assets can be distributed through lump-sum payments, annuity purchases, or rollovers. While lump-sum payments provide immediate access to funds, they may have tax implications and lack long-term planning benefits. Annuity purchases offer a steady income stream in retirement but are less flexible. Rollovers allow for tax-deferred savings continuity and investment choice control through transfers to qualified plans or IRAs. The retirement plan termination process also involves filing required documents with regulatory agencies, such as the Internal Revenue Service (IRS) and the Department of Labor (DOL). This may include submitting a final Form 5500, as well as other forms necessary to report the termination and distribution of plan assets. During the retirement plan termination process, the plan trust must also be terminated. This involves ensuring all plan assets have been distributed to participants and beneficiaries, as well as resolving any outstanding liabilities or expenses related to the plan. Once all assets have been distributed and obligations fulfilled, the plan sponsor can formally dissolve the trust and cease its existence. Even after the retirement plan has been terminated, plan sponsors may still have certain compliance responsibilities. These can include retaining plan records for a specified period, addressing any post-termination audits or inquiries from regulatory agencies, and ensuring that any required tax filings or reports have been completed accurately and submitted on time. Remaining vigilant in post-termination compliance helps protect both the plan sponsor and participants from potential legal issues or penalties. Participants have the right to receive clear and concise information about their distribution options during plan termination. This includes details about the available choices, the tax implications of each option, and any potential fees or penalties associated with the distribution. Participants also have the right to roll over their plan assets to another qualified retirement plan or IRA during plan termination. This option can help preserve the tax-deferred status of the funds, maintain investment control, and facilitate the continuation of retirement savings. During plan termination, participants are entitled to the protection of their vested plan benefits. This means that employers cannot reduce or eliminate the vested portion of a participant's account balance as a result of the termination. In the case of defined benefit plans, participants may be eligible for insurance coverage provided by the Pension Benefit Guaranty Corporation (PBGC), a federal agency that guarantees certain pension benefits in the event of plan termination. This coverage can provide financial security for participants if their employer is unable to fulfill its pension obligations. One potential issue in retirement plan termination is participant confusion or dissatisfaction with the available distribution options. This can result from inadequate communication or a lack of understanding about the implications of each option, leading to suboptimal choices for long-term financial planning. Another challenge during retirement plan termination is ensuring legal and regulatory compliance. Navigating the complex rules and regulations surrounding retirement plans can be difficult, and failure to comply can result in penalties or legal action against the plan sponsor. Properly disbursing plan assets to participants during termination can also pose challenges, as it requires accurately calculating account balances, withholding taxes, and processing payments in a timely manner. Mistakes in this process can lead to delays or errors in distribution, causing frustration for participants. Plan sponsors have fiduciary responsibilities to act in the best interests of plan participants, even during plan termination. This includes making prudent decisions regarding the distribution of assets, ensuring regulatory compliance, and providing accurate and timely information to participants. Retirement plan termination is a complex process that involves notifying participants, distributing plan assets, filing required documents with regulatory agencies, and ensuring participant rights are protected. It is crucial for plan sponsors and participants to understand the termination process to navigate it effectively. Effective plan management and regulatory compliance play a significant role in avoiding retirement plan termination. By properly managing a retirement plan and adhering to all applicable regulations, plan sponsors can mitigate the risk of termination and provide a stable, long-lasting retirement savings vehicle for their employees. To better navigate the complexities of retirement plan termination and ensure the best possible outcomes for all parties involved, it is recommended that employers and employees seek the assistance of professional retirement planning services.What Is Retirement Plan Termination?

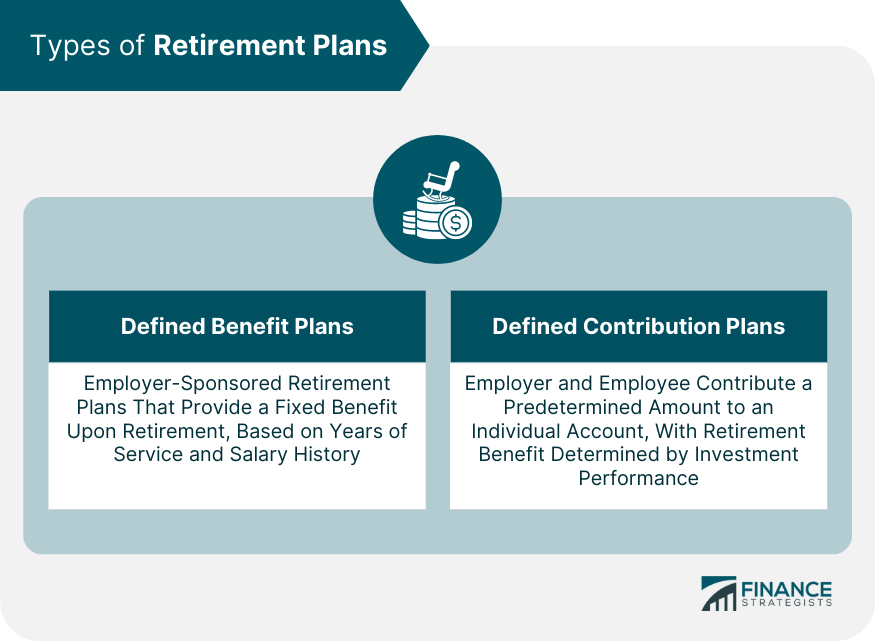

Types of Retirement Plans

Defined Benefit Plans

Defined Contribution Plans

Reasons for Retirement Plan Termination

Company Restructuring or Bankruptcy

Plan Merger or Acquisition

Plan Underperformance or Mismanagement

Regulatory Compliance Issues

Changes in Company Strategy or Objectives

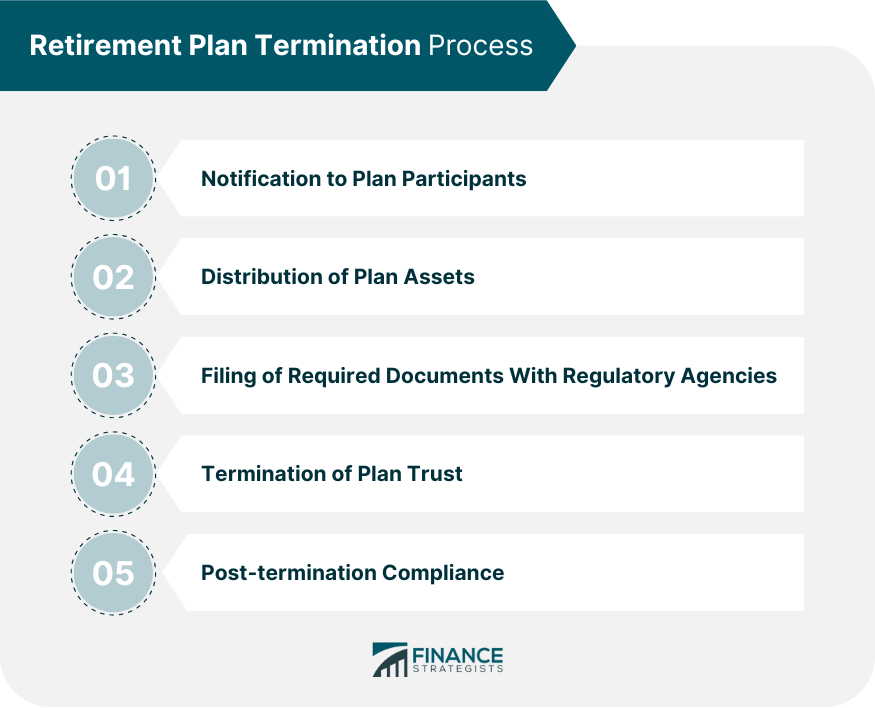

Retirement Plan Termination Process

Notification to Plan Participants

Distribution of Plan Assets

Filing of Required Documents with Regulatory Agencies

Termination of Plan Trust

Post-termination Compliance

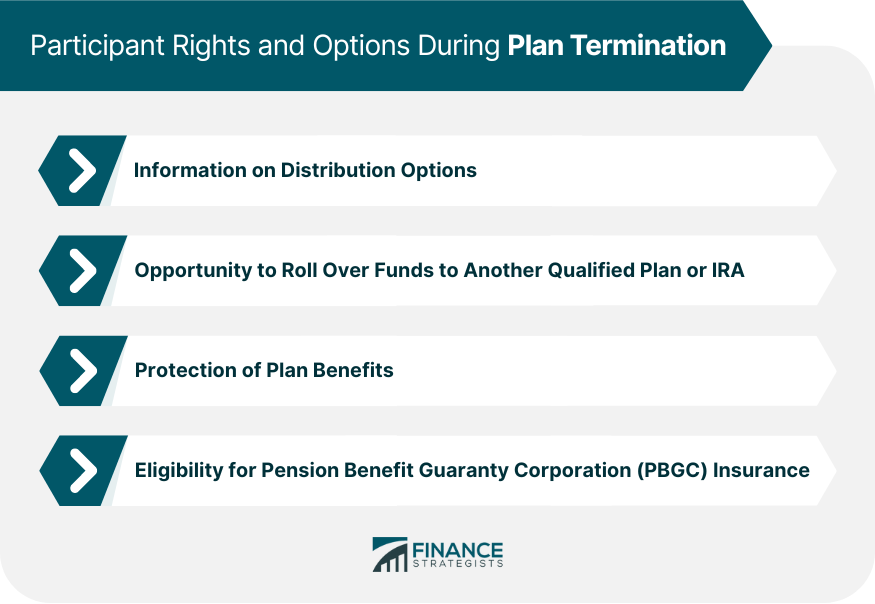

Participant Rights and Options During Plan Termination

Information on Distribution Options

Opportunity to Roll Over Funds to Another Qualified Plan or IRA

Protection of Plan Benefits

Eligibility for PBGC Insurance

Potential Issues and Challenges in Retirement Plan Termination

Participant Confusion or Dissatisfaction with Distribution Options

Legal and Regulatory Compliance

Disbursement of Plan Assets

Plan Sponsor Fiduciary Responsibilities

Final Thoughts

Retirement Plan Termination FAQs

Retirement plan termination refers to the process of ending a retirement plan, either voluntarily or involuntarily, and distributing the remaining plan assets to participants and beneficiaries. Understanding the process is crucial for both employers and employees, as it impacts financial planning, retirement security, and tax implications.

Some common reasons for retirement plan termination include company restructuring or bankruptcy, plan merger or acquisition, plan underperformance or mismanagement, regulatory compliance issues, and changes in company strategy or objectives.

The retirement plan termination process involves notifying plan participants, distributing plan assets through lump-sum distributions, annuity purchases, or rollovers to other qualified plans or IRAs, and filing required documents with regulatory agencies, such as the IRS and the DOL.

During retirement plan termination, participants have the right to receive clear information on distribution options, the opportunity to roll over funds to another qualified plan or IRA, protection of their vested plan benefits, and, in the case of defined benefit plans, eligibility for PBGC insurance.

Potential challenges during retirement plan termination can include participant confusion or dissatisfaction with distribution options, ensuring legal and regulatory compliance, disbursing plan assets accurately and timely, and fulfilling plan sponsor fiduciary responsibilities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.