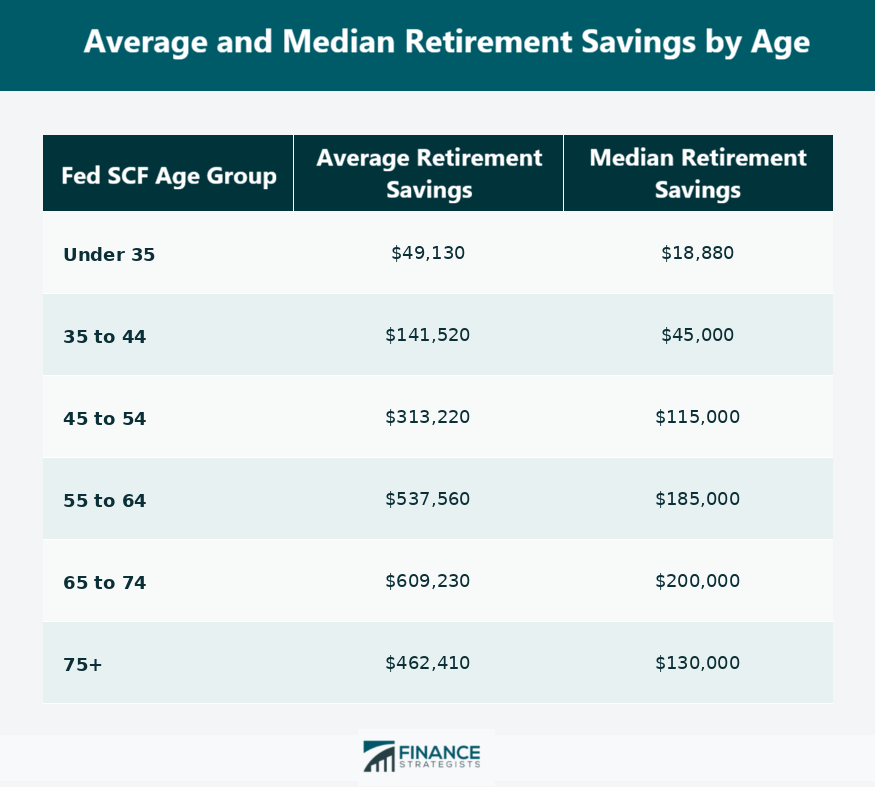

Regardless of where you are in your career, life stage or financial plans, comparing your retirement savings with national benchmarks can help you gauge whether you are on track to meet your goals. That context is especially valuable in 2026 as inflation, interest rates and market uncertainty continue to affect how Americans save, invest and plan for retirement. The average retirement savings balance is calculated by adding all balances together and dividing by the number of households. As such, high-balance households can skew that number upward, often making the average larger than what typical households have actually saved. This is where the median rate comes in handy, since it shows the midpoint where half of households have more and half have less. Using both the average and median retirement savings figures can give you a more nuanced picture of where you stand. These metrics can inform your decisions when setting contribution rates, reviewing your retirement timeline or gauging whether you need adjustments. It can also help you avoid two common mistakes if you were to look at one metric alone: panicking because you are below average, or assuming you are on track just because you are above the median. You should always treat these figures as reference points rather than one-size-fits-all targets. Your retirement needs depend on your income, expenses, debt, tax situation, retirement age, expected Social Security benefits, pension income, health, family situation and desired lifestyle. While a benchmark tells you where you stand compared with others, your retirement plan should be based on how much income you will actually need and how long your savings may need to last. The retirement savings numbers mentioned come from the Federal Reserve’s most recent Survey of Consumer Finances. The SCF provides a detailed look at U.S. household finances, including assets, debts, income and retirement accounts. The survey is conducted every three years and is widely used by researchers, policymakers and financial professionals to analyze how American families save and build wealth. The numbers below reflect households with retirement accounts and show both average and median balances by the Fed’s published age groups. Because the Federal Reserve uses brackets rather than exact decade-by-decade categories, the sections that follow use the closest available Fed age groups as reference points. Retirement savings balances vary, even among people in the same age group. Aside from your life stage, your balance is shaped by income, contribution rates, account type, and market performance. This is the foundation of your retirement savings, and it determines how much room you have to contribute. High earners may have the flexibility to save more, but it doesn’t automatically mean higher savings. Lifestyle inflation, debt, housing costs, family obligations and bad financial habits can limit your progress. So consistency is key, regardless of how much you earn. Even small contributions become significant over time with compounding. A person saving 5% of their income is more likely to have a very different outcome than someone saving 10%, 15% or more, even if they have similar earnings. Your contribution rate is crucial because you have more control over it. Increase your contributions gradually to make it more manageable. Keep your contribution rate proportional to any increase in income. Say you get a 5% salary increase; your contribution rate should increase by at least 5%. And always aim to contribute enough to trigger the full employer match at work. Account types affect your returns and how they are taxed. Traditional 401(k) and IRAs allow pre-tax contributions, and withdrawals are taxed later. Roth accounts use after-tax contributions, so qualified withdrawals in retirement are generally tax-free. Taxable brokerage accounts are not subject to RMDs and early withdrawal penalties, but they don’t enjoy the same tax advantages. You can use multiple account types for flexibility. For example, having both traditional and Roth accounts may give you more control over taxable income in retirement. The best mix depends on your income, tax bracket, employer plan and expected retirement timeline. Strong market periods can raise retirement savings portfolios quickly, while downturns can temporarily reduce them even if you continue contributions. This is why your retirement balance can vary from year to year. And because markets move in cycles, it’s crucial not to judge your savings progress based on a single year. You should think long term and focus on consistent contributions, diversification and an allocation that fits your age, risk tolerance and timeline. Market conditions matter, but your behavior during swings is more important. Remember, time in the market is always better than timing the market. Play the long game and be strategic. This question requires more than comparing your retirement savings to the average or median of your age group. Again, those figures provide context, but they do not reflect your desired retirement age, projected expenses, income sources, debt, taxes, health or retirement lifestyle. A better starting point is to estimate how much annual income you may need in retirement, then compare that to reliable income sources, such as Social Security, pensions, annuities and other assets. From there, review whether your current savings rate and investment strategy are likely to close the gap by your target retirement age. You can use this retirement calculator to make things easier. Depending on the result, you may need to increase contributions, delay retirement or make any other adjustments. What’s important is to regularly review and update your retirement plan. If you are behind on your retirement savings, the most obvious step is to increase contributions where possible. A priority could be to capture the full employer match in your workplace plan. Don’t waste this part of your compensation. You should also take advantage of catch-up contributions to 401(k)s or IRAs if you are 50 or older. Automation can help turn saving into a default behavior. Set up automatic contributions to a retirement or brokerage account as soon as you receive your paycheck to reduce reliance on discipline. If cash flow is tight, start small and step up your savings. For example, by increasing your contribution by $20 more each month, you’ll have saved an additional $1,560 in one year. Catching up may also require reviewing the rest of your finances. Pay down high-interest debts to free up future cash flow. Ensure your investment allocation is positioned for long-term growth and not too conservative for your timeline. You can also optimize your finances without cutting expenses. The goal is not to fix everything at once. Look for several manageable changes and be consistent. Retirement planning is not set-it-and-forget-it. Your income and expenses change, markets rise and fall, and your retirement goals may evolve over time. A savings balance that looked sufficient five years ago may need a second look. Regular reviews help you identify gaps early, while there’s still time to adjust. A good review should include your current balance, contribution rate, investment allocation and your projected retirement date, income sources and expenses. The median and average retirement savings by age are useful references for gauging your retirement readiness. Use these benchmarks as context, but build or adjust your retirement plan based on your actual income needs, timeline, contribution rate, investment strategy and desired lifestyle. For more information and tailored advice, consider working with a financial advisor or retirement counselor. Author's note: This article was originally published in Forbes.com. The Average and Median Retirement Savings table was created with the help of AI.Why Knowing The Average Retirement Savings Can Help

Average Retirement Savings By Age

20s Age Group

30s Age Group

40s Age Group

50s Age Group

60s Age Group

70s Age Group

80s Age Group

90s Age Group

Factors Which Affect Your Savings Balance

Income Levels

Contribution Rates

Retirement Account Types

Market Conditions

Are You On Track To Retire In 2026?

How To Catch Up On Retirement Savings

Monitoring Your Savings Progress

Average Retirement Savings by Age in 2026 FAQs

Sources vary about the exact figure. According to one analysis of the latest Fed SCF data, 9.3% of U.S. households had more than $500,000 in retirement accounts, while another puts the figure at $900,000.

No, it’s not too late to start saving at 50 but you may need to be more intentional about it. Focus on increasing contributions, using catch-up contributions when eligible, and maximizing employer match to boost your savings. It’s also a good idea to pay down your debt, especially high-interest ones.

While it’s ideal to be debt-free in retirement, you don’t want to sacrifice savings. You should tackle high-interest debt first because it eats away too much of your funds, which could otherwise be used for savings and investments.

That depends on your income, lifestyle and retirement goals, but the latest Fed SCF reports that the median retirement savings for people in their 40s range from $45,000 to $115,000. Use those figures as benchmarks, then compare them with your own retirement timeline and expected income needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.