According to the Partnership Act, no interest is provided on capital, but if it is agreed upon among the partners, it will be provided at an agreed rate. Interest on capital is not an expense of the business. That is to say, it is not deducted from the total income to arrive at the net income. It is a part of the profit-sharing scheme. The journal entry for interest on capital is as follows: To record each partner's drawings, a separate drawing account is maintained for each individual. Generally, a maximum withdrawal limit is established. According to the Partnership Act, no interest on drawings is charged unless there is an agreement among the partners to the contrary. If the partners have agreed to charge interest on drawings, the entry is made as follows: According to the Partnership Act, no partner is entitled to any salary. However, if there is an agreement in place, a partner may be allowed a salary for their work to the firm. A partner's salary is not an expense of the business (i.e., it is not deducted from the total income to arrive at the net income). It is a part of the profit-sharing scheme. The journal entry for partner's salary is made as follows: Sometimes, commission is allowed to the partners. The commission is transferred to the partner's account by way of the following journal entry: The profit or income of the partnership is distributed among the partners. The following journal entry is passed to transfer the profit to a partner's account: The loss of partnership is suffered by the partners. The following journal entry is made to transfer the loss to the partner's account:Interest on Capital

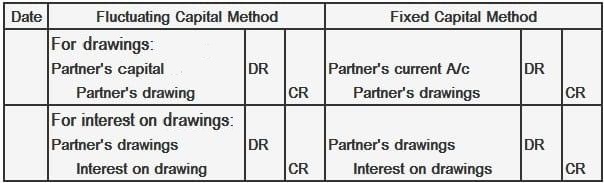

Drawings

Partner's Salary

Partner's Commission

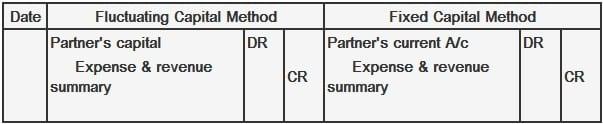

Partner's Profit or Income

Partner's Loss

Journal Entries Under Fluctuating and Fixed Capital Methods FAQs

Yes, the partner can claim interest on loan from the firm. There is no restriction in law.

No, a business cannot claim interest on its capital. Only partners can do so if they agree with each other.

Interest on drawings is not an expense of the business. It is a part of profit sharing scheme between partners.

If there is an agreement among the partners to charge interest on drawings, an entry should be made in the books of accounts.

The partner's salary is not treated as an expense of business.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.