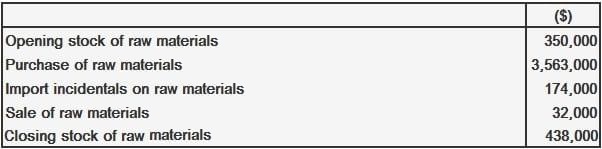

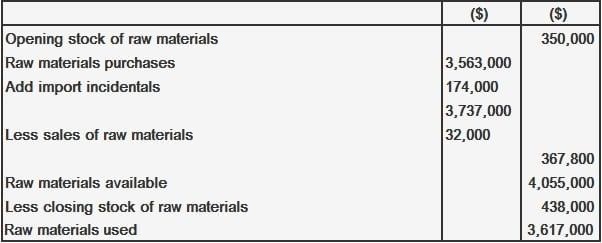

A direct material is any commodity that enters into and becomes a constituent element of a product. Thus, cotton is a direct material for textile goods, leather for shoes, wood (or steel or plastic) for furniture, and so on. Some products have more than one direct material. For example, biscuits are made not only of flour but also sugar, milk, oils, and other ingredients. Another name for direct materials is raw materials. To determine the cost of direct materials used in a specific year, the value of unused raw materials in-store at the beginning of the year (i.e., opening stock) should be added to the value of the raw materials bought during the year and from the total. From this, deduct the value of unused raw materials at the end of the year (i.e., closing stock). This procedure is shown as follows: If any carriage costs are incurred on purchases of raw materials, such costs should be added to the value of the materials bought in the year. Additionally, if any material is returned to suppliers (i.e., returns outward), such returns should be deducted from the purchase figure. This yields the net value of raw materials bought in the year. If, in the above example, we are told that carriage inward expenses amounted to $17,400 and returns outwards to $5,900, the value of raw material used will be computed as follows: Sometimes, raw materials are imported from another country. In such cases, expenses such as import duties, sea or air freight, marine insurance, and clearing charges are incurred. These import-related expenses are added to the cost of raw materials bought in the same manner as carriage inward. If part of the imported raw material is not found to be satisfactory (or is in excess of needs), it may be too expensive and inconvenient to return that part to the overseas supplier. Such material is often sold locally. The proceeds from the sale of raw materials are deducted from the purchase price in the same manner as returns inward. An indirect material is a material that indirectly forms part of the finished product; it cannot be directly charged to the unit or the order. Glue, nails, rivets, and other such items are examples of indirect materials. To calculate the unit cost of indirect materials, the total cost is divided by the number of units manufactured. The following figures were taken from the ledger of John Fertilizers Co., a prominent importer of raw materials: The cost of raw materials used by John Fertilizers Co. is calculated as follows:Definition and Explanation

Direct Materials Cost

Example

Indirect Materials Cost

Example

Solution

Direct and Indirect Materials Cost FAQs

A direct material is any commodity that enters into and becomes a constituent element of a product.

Direct materials are the physical items built into a product. For example, cotton is a direct material for textile goods, leather for shoes, wood (or steel or plastic) for furniture, and so on.

An indirect material is a material that indirectly forms part of the finished product; it cannot be directly charged to the unit or the order.

Indirect materials are goods that are part of the entire manufacturing process but are not integrated into the final product. Glue, nails, rivets, and other such items are examples of indirect materials.

To calculate the unit cost of indirect materials, the total cost is divided by the number of units manufactured.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.