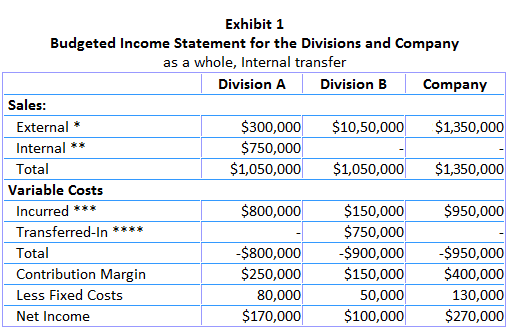

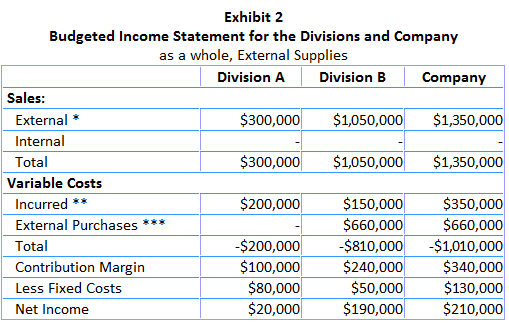

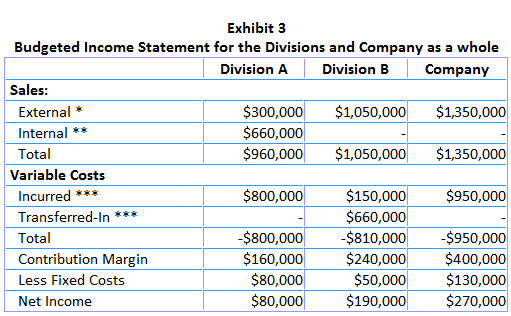

Suppose that a company has two divisions: Division A and Division B. Division A sells to both Division B and other outside customers. However, Division B buys from only Division A. The following unit costs were incurred by Division A for the coming year: Suppose that for the year, Division A produced 40,000 units, 30,000 of which were sold to Division B for $25 each. The outside sales were for $30. Also, the fixed manufacturing costs for the year were $80,000. When Division B receives the units from Division A, it processes them further before selling them to customers. The variable unit costs of Division B are $5 and its fixed costs for the year are $50,000. Division B sells all the units received from Division A at $35 each. * 10,000 units x $30 = $300,000 and 30,000 units x $35 = $1,050,000 ** 30,000 units x $25 = $750,000 *** 40,000 units x $20 = $800,000 and 30,000 units x $5 = $150,000 **** Transferred-in costs are the same as internal sales Exhibit 1 shows how transfer pricing affects each division's income statement and the company as a whole. The 30,000 units transferred from Division A to Division B is shown as $750,000 of internal sales for Division A and as $750,000 of transferred-in cost to Division B. Both amounts are not considered when preparing the overall company income statement. This is done so as to provide the external users of financial statements with information relating to the economic activities of the company with outside parties and not internal transfers. Now suppose that Division B is allowed to buy from outside suppliers. An outside supplier has offered to supply the same type of units for $22 to Division B. Division A does not agree to reduce its price even though it has no alternative use of its production capacity. * 10,000 units x $30 = $300,000 and 30,000 units x $35 = $1,050,000 ** 10,000 units x $20 = $200,000 and 30,000 units x $5 = $150,000 *** 30,000 units x $22 = $660,000 Exhibit 2 shows that Division B increased its net income by $90,000 when it purchased from an external supplier. However, the profit of Division A and the company as a whole declined when Division B purchased from an outside supplier. * 10,000 units x $30 = $300,000 and 30,000 units x $35 = $1,050,000 ** 30,000 units x $22 = $660,000 *** 40,000 units x $20 = $800,000 and 30,000 units x $5 = $150,000 **** Transferred-in costs are the same as internal sales Finally, assume that Division A is willing to negotiate a transfer price with Division B for $22. Exhibit 3 shows the income statement for each division and the company as a whole with the negotiated transfer price. Comparing Exhibits 1 and 3, the overall income of the company remains the same when there are internal transfers and the transfer price is reduced from $25 to $22. However, the profit of Division B increases, and that of Division A decreases. Division B is satisfied to have outside competition since its net profit increases under both the alternatives. Hence, transfer prices influence the profitability of both the buying and selling divisions. Performance evaluation of the divisional managers can also be done in a realistic manner. The company-wide impact of transfer prices should be carefully examined to fully assess the results of the decisions involved in transfer pricing.

Transfer Pricing Illustrated FAQs

Transfer pricing is the process of establishing the price at which one business unit within a company transfers goods or services to other business units within the same enterprise. It also refers to the similar process of setting the prices charged by a parent organization for various products and services provided to its subsidiary companies.

There are three types of transfer pricing techniques. These are (1) comparable uncontrolled price method, (2) resale price method, and (3) cost-plus method.

The internal transfer price refers to the amount charged by one department of a business to another for goods or services. This is also called as an intra-organizational transfer price. On the other hand, the external transfer price usually determines how much the company should charge from its customers for transferring a product or service to them. This is also called an inter-organizational transfer price.

There are several factors that can affect internal transfer pricing decisions including market considerations, legal restrictions, tax implications, accounting practices, agreed divisional performance objectives and bargaining strength of the divisions involved in the transfer.

Transfer prices can reduce the amount of internal competition within a company, thereby aiding in better allocation of resources across different organizational units. It also helps in reducing inter-divisional conflict and increasing overall profitability.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.