The procedures available for determining the profit or loss on contracts under different circumstances are summarized in this article. For contracts completed during the accounting year, the full contract price, whether payable in a lump sum on the completion of the contract or payable in installments, is debited to the contractee personal account and credited to the contract account. The difference between the total of the two sides of the contract account is transferred to the profit and loss account of the contractor by way of profit or loss. Sometimes, under the terms of the agreement, the contractor undertakes to rectify the defects, if any, in the contract work that may arise during a specified period (known as the maintenance period) after the date of the completion of the contract. The amount of profit or loss on contracts in such cases should be ascertained only after making a sufficient provision for the cost of maintenance that is expected during the maintenance period. As a general rule, profits on incomplete contracts should not be credited. A number of arguments are given against calculating profits on incomplete contracts: However, it is counter-argued that when profit on incomplete contracts is included in the profit and loss account, undue fluctuations in the profits and dividends paid can be avoided. Also, some contracts may take several years to complete, which means that if profits are calculated only on completion, it will seem like the entire amount was earned in one year, which is incorrect. Therefore, profits on incomplete contracts should be calculated very cautiously. Only a portion of these profits may be credited to the profit and loss account. The computation of profit on incomplete contracts has two aspects: For this purpose, the value of certified work and the cost of uncertified work at the end of the accounting period is credited to the contract account. The amount of notional profit is calculated as follows: The entire amount of notional profit at the end of the accounting period is not transferred to the profit and loss account. Given the future uncertainties involved in contract work, only a portion of the notional profit is transferred to the profit and loss account. The remainder is kept by way of a provision to cover future contingencies. The following principles are generally followed to ascertain the proportion of notional profit to be transferred to the profit and loss account. These are contracts that have just commenced or where only a small portion of the contract has been finished. For such contracts, it is not prudent to take credit for any profit made because it is impossible to see the future position of such contracts clearly. The entire amount of notional profit on such contracts is kept by way of provision for contingencies. It is transferred to the credit of the work-in-progress account so as to bring it down to its actual cost. A contract is generally said to have made appreciable progress if at least 1/4 of the contract has been completed. The proportion of the notional profit to be transferred to the profit and loss account in respect of such contracts is calculated as follows: These are contracts that are nearing completion and for which the future costs to be incurred on their completion can reasonably be estimated. In this case, the amount of profit to be transferred to the profit and loss account is determined based on estimated profit. Estimated profit for contracts nearing completion is the difference between the contract price and the estimated cost of the contract on completion. Estimated profit can be calculated as follows: The calculation of the estimated cost of the contract on completion is as follows: Notably, only a proportion of the estimated profit is transferred to the profit and loss account, leaving the balance to guard against future contingencies. The proportion of estimated profit to be transferred to the profit and loss account can be calculated using any of the following: When an incomplete contract reveals a loss, the whole amount of the loss must be charged to the profit and loss account of the accounting year.1. Profit on Completed Contracts

2. Profit on Incomplete Contracts

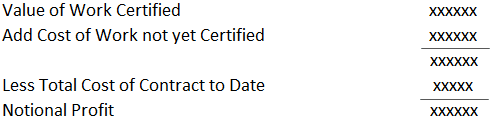

(a) Calculating Notional Profit at the End of the Accounting Period on Incomplete Contracts

(b) Calculating the Proportion of Notional Profit to Be Transferred to Profit and Loss Account

(i) Incomplete Contracts With Little Progress

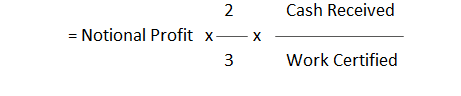

(ii) Incomplete Contracts With Appreciable Progress

(iii) Incomplete Contracts Nearing Completion

3. Loss on Incomplete Contracts

How to Calculate Profit and Loss on Contracts FAQs

For contracts completed during the accounting year, the full contract price, whether payable in a lump sum on the completion of the contract or payable in installments, is debited to the contractee’s personal account and credited to the contract account.

Therefore, profits on incomplete contracts should be calculated very cautiously. Only a portion of these profits may be credited to the profit and loss account.

These are contracts that have just commenced or where only a small portion of the contract has been finished. For such contracts, it is not prudent to take credit for any profit made because it is impossible to see the future position of such contracts clearly.

A contract is generally said to have made appreciable progress if at least 1/4 of the contract has been completed.

When an incomplete contract reveals a loss, the whole amount of the loss must be charged to the profit and loss account of the accounting year.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.