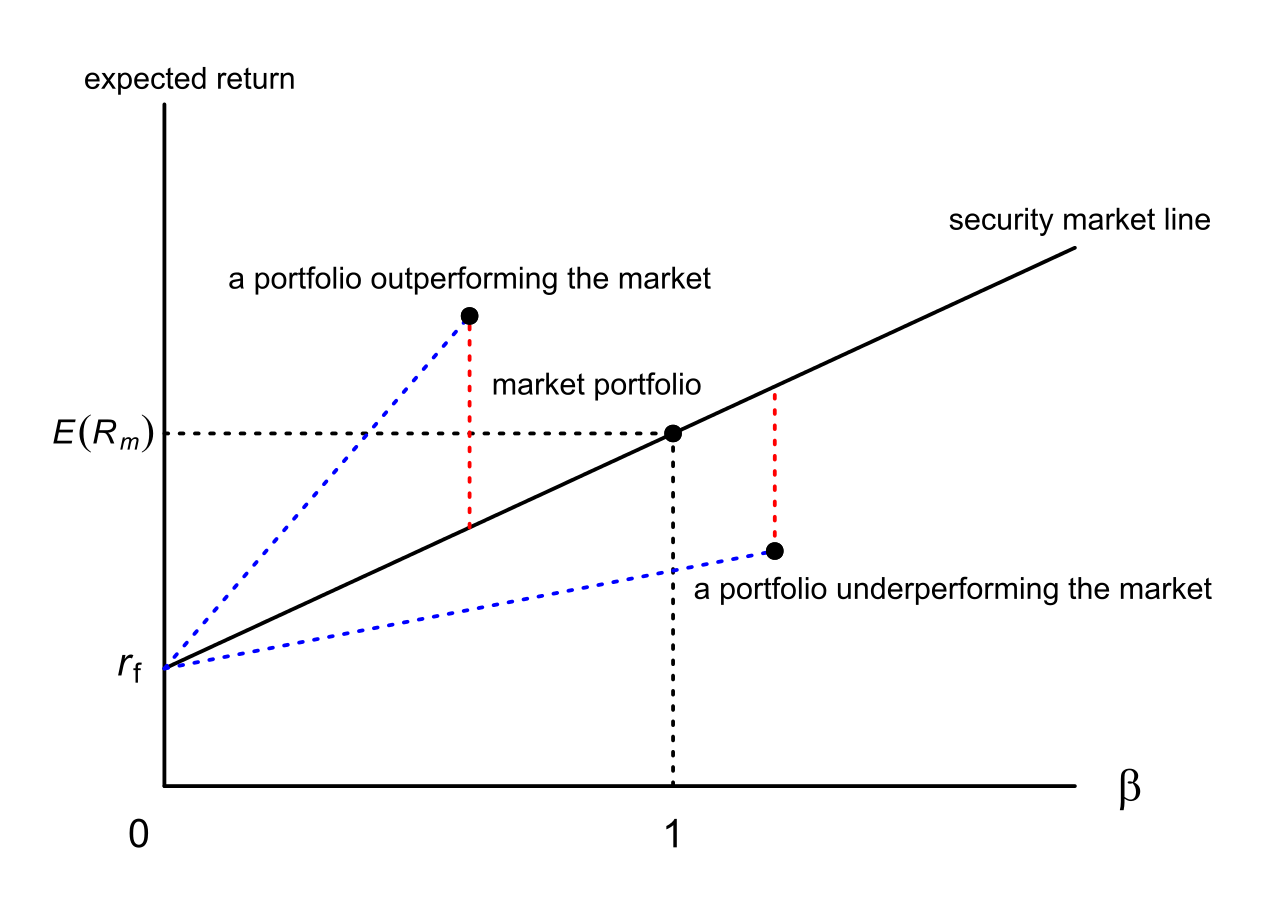

Valuation is a process by which analysts determine the present or expected worth of a stock, company, or asset. The purpose of valuation is to appraise a security and compare the calculated value to the current market price in order to find wise investments. While the current market price is said to reflect all variables (including irrational behavior), valuation models will only factor in a few variables. This is why there are so many different methods of valuation. This article will cover three of the most popular valuation models: The Dividend Discount Model, or DDM, is one of the most common valuation models. This model values a share by estimating the present value of future dividends a stock will pay. Because investors expect to earn interest on their money over time, money today is worth more than the same value paid out at a later date. This is why future payouts are "discounted" when computing their value today. The rate at which future dividends are discounted is known as the weighted average cost of capital. The Weighted Average Cost of Capital, or WACC, is the "opportunity cost" of what the investor's money could have made if it were invested elsewhere. The Dividend Discount Model also factors in an estimated perpetual increase of the dividend payout made over time based on historical increases of the dividend payout. The present value of future dividends is equal to the estimated value of the stock. If the present value of future dividends calculated by the DDM is greater than the current price of the stock, then the DDM suggests it is a buying opportunity. A major limitation of the Dividend Discount Model is that it can only be used if the company pays a dividend and the dividend returns are stable and predictable. Discounted Cash Flow Model, or DCF values a company based on its future cash flows discounted by the investor's expected rate of return, which is then used to calculate the stock price. The Discounted Cash Flow Model can be used even if a company doesn't pay a dividend or has unpredictable dividend returns. To calculate the value of a share using the Discounted Cash Flow Model, add up the value of future earnings, then discount the earnings by the weighted average cost of capital, or WACC. Then, subtract net debt from the enterprise value to compute the company's fair value and divide by the number of outstanding shares to calculate the value of a share. The formula for DCF is as follows: If the estimated value of a share using the Discounted Cash Flow Model is greater than the current value of a share, the DCF model suggests it is a buying opportunity. The weakness of this model is that it relies entirely on future cash flow estimates, which are unknown. Additionally, appraising the cash flows and discount rates incorrectly can lead to inaccurate conclusions on the attractiveness of the investment. The Capital Asset Pricing Model, or CAPM, calculates the value of a security based on the expected return relative to the risk investors incurs by investing in that security. To calculate the value of a stock using CAPM, multiply the volatility, known as "beta" by the additional compensation for incurring risk, known as the "Market Risk Premium," then add the risk-free rate to that value. The formula for CAPM is as follows: Expected return of the investment = the risk-free rate + the beta of the investment times the expected return on the market - the risk free rate which is the market risk premium. For each additional increment of risk incurred, the expected return should proportionately increase. If a security is found to have a higher return relative to the additional risk incurred, then the CAPM model suggests that it is a buying opportunity. Like all valuation models, CAPM has its limitations since some assumptions it uses are idealistic. For example, Beta coefficients are unpredictable, change over time, only reflect systematic risk rather than total risk. Despite its shortcomings, this model is very popular for valuing securities.Valuation Definition

Dividend Discount Model (DDM)

Discounted Cash Flow Model (DCF)

Capital Asset Pricing Model (CAPM)

Valuation Methods FAQs

Valuation is a process by which analysts determine the present or expected worth of a stock, company, or asset.

The purpose of valuation is to appraise a security and compare the calculated value to the current market price in order to find wise investments.

The three primary Valuation Methods are the dividend discount model (DDM), the discounted cash flow model (DCF), and the capital asset pricing model (CAPM).

While the current market price is said to reflect all variables (including irrational behavior), valuation models will only factor in a few variables.

The Discounted Cash Flow (DCF) valuation method calculates the present value of future cash flows by discounting them using an appropriate rate. This rate represents the cost of capital and takes into account both the risk and time value of money.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.