The equity risk premium is the additional return that investors expect to receive for investing in a company's stock rather than in risk-free securities, such as government bonds. The ERP compensates investors for the additional risk associated with equity investments. The ERP is a crucial component in determining the cost of equity capital, as it reflects the risk associated with investing in a particular company or market. By understanding the ERP, investors can make informed decisions about the expected return on their investments. The ERP plays a vital role in finance, as it helps investors determine the appropriate return they should expect when investing in stocks. It also serves as a key input in various financial models, such as the Capital Asset Pricing Model (CAPM), which is used to estimate the cost of equity capital. There are several methods for calculating the ERP, including the historical method, the dividend discount model, and the implied ERP method. Each method has its advantages and limitations, and investors may use different approaches depending on their specific needs and investment objectives. The historical method calculates the ERP based on the difference between the historical returns of stocks and risk-free securities, such as government bonds. This method assumes that the past performance of stocks is indicative of their future performance. The dividend discount model calculates the ERP by estimating the expected future cash flows from a stock and discounting them back to the present value. This method relies on assumptions about future growth rates and dividend payouts, which may be subject to change. The implied ERP method is a way to calculate the equity risk premium by using market prices and implied volatility. This method assumes that the market is efficient and incorporates all relevant information. It calculates the expected returns of stocks by analyzing the market prices of options and futures contracts, and it compares these expected returns to the risk-free rate. The difference between the expected returns and the risk-free rate is the implied ERP. There are several factors that can influence the ERP, including macroeconomic conditions, market volatility, and investor sentiment. Understanding these factors can help investors anticipate changes in the ERP and adjust their investment strategies accordingly. Economic conditions, such as GDP growth, inflation, and interest rates, can have a significant impact on the ERP. For example, during periods of high economic growth, investors may require a lower ERP as they perceive stocks to be less risky. Increased market volatility can lead to higher ERPs, as investors demand greater compensation for the increased risk associated with fluctuating stock prices. Conversely, during periods of low volatility, investors may be willing to accept a lower ERP. Analyzing historical ERP trends can provide valuable insights into how the ERP has evolved over time, as well as the factors that have contributed to its fluctuations. This information can help investors better understand the relationship between risk and return in the equity market. Historically, the ERP has exhibited significant variability, with periods of both high and low premiums. These fluctuations are often driven by changes in economic conditions, market volatility, and investor sentiment. By analyzing historical ERP data, investors can gain insights into how the ERP has responded to different market conditions and economic environments. This information can be useful in informing investment decisions and developing appropriate risk management strategies. Current ERP estimates can provide investors with valuable information about the level of risk and expected return in the equity market today. These estimates can vary across industries and regions, reflecting the diverse nature of equity investments. Various sources provide current ERP estimates, which can be useful for investors seeking to understand the level of risk and potential return in the equity market. However, it is important to recognize that these estimates are subject to change, as they are influenced by a wide range of factors. The ERP can vary significantly across different industries and regions, reflecting differences in risk profiles and expected returns. For example, industries with higher levels of risk, such as technology or biotechnology, may have higher ERPs compared to more stable industries, such as utilities. Similarly, ERPs in emerging markets may be higher than those in developed markets due to increased risks associated with investing in these regions. Despite its widespread use in finance, the concept of the ERP has faced several criticisms. These critiques focus on the conceptual and methodological aspects of the ERP and can have implications for investors relying on the ERP for investment decision-making. Some critics argue that the ERP is based on the assumption that investors are risk-averse and require a premium for investing in riskier assets, such as stocks. However, this assumption may not always hold true, as some investors may be risk-seeking or may invest in stocks for reasons other than expected returns, such as diversification or long-term growth potential. The various methods used to calculate the ERP, such as the historical method or the dividend discount model, each have their own limitations and assumptions. These limitations can lead to inaccuracies in the estimated ERP, potentially resulting in misleading conclusions about the level of risk and expected return in the equity market. The equity risk premium is an essential concept in finance, as it helps investors determine the appropriate return they should expect when investing in stocks. By understanding the factors that affect the ERP, as well as the various methods used to calculate it, investors can make informed decisions about their investments and effectively manage risk. Despite the criticisms surrounding the ERP, it remains a crucial component of investment decision-making. By considering the ERP and its potential limitations, investors can better assess the level of risk associated with their equity investments and make more informed decisions about their investment strategies.Definition of Equity Risk Premium (ERP)

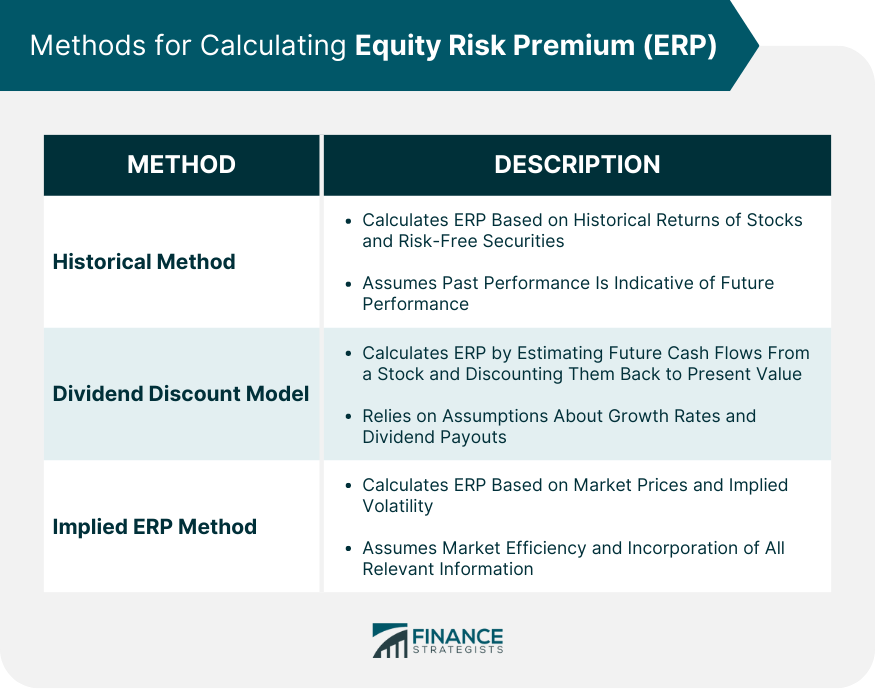

Calculation of Equity Risk Premium

Historical Method

Dividend Discount Model

Implied ERP Method

Factors Affecting ERP

Macroeconomic Conditions

Market Volatility

Historical ERP

ERP Trends over Time

Analysis of Historical ERP Data

Contemporary ERP

Current ERP Estimates

Variations in ERP Across Industries and Regions

Criticisms of Equity Risk Premium

Conceptual Criticisms

Methodological Criticisms

Conclusion

Equity Risk Premium FAQs

Equity Risk Premium (ERP) is the excess return that investors expect from investing in stocks over a risk-free investment, like bonds.

The Equity Risk Premium can be calculated by subtracting the risk-free rate of return from the expected return of the stock market.

Some factors affecting ERP include inflation, economic growth, company earnings, and interest rates.

ERP helps investors assess the risk-reward tradeoff in investing in stocks and make informed investment decisions.

Criticisms of ERP include that it is difficult to accurately predict, can vary over time, and may not account for all relevant risk factors.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.