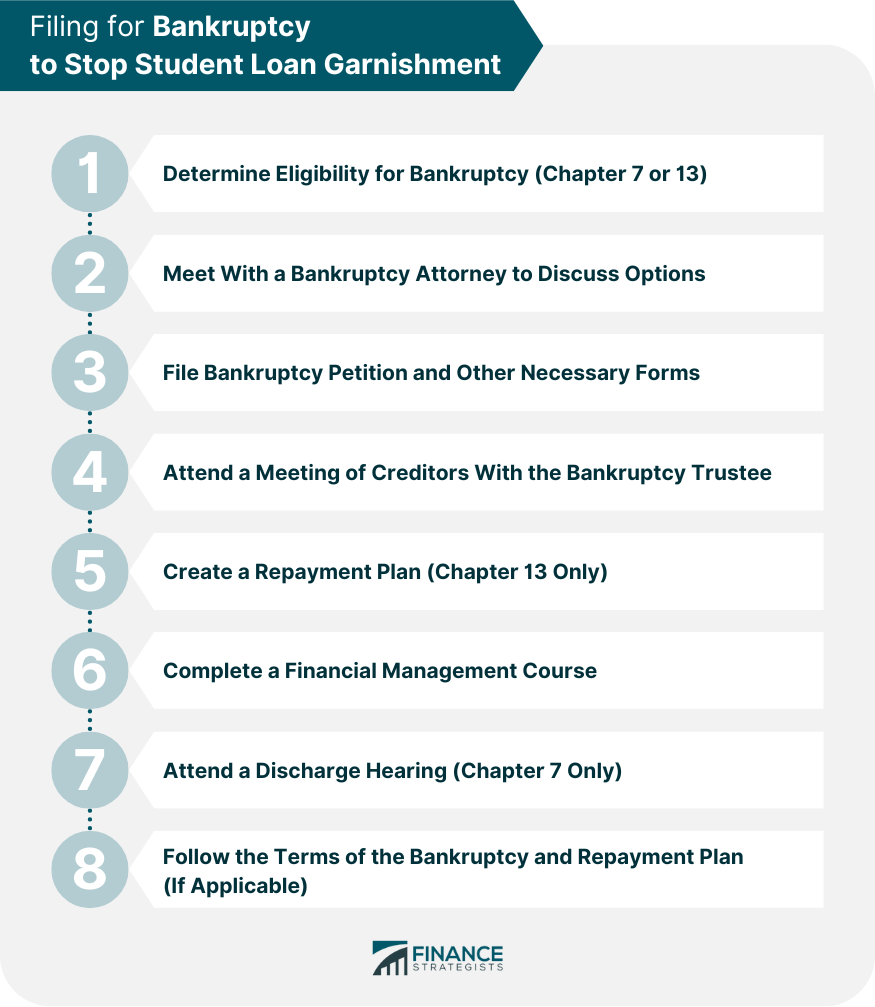

Yes, filing for bankruptcy can and will stop student loan garnishment, including wage garnishment and bank account attachment, by implementing an automatic stay that halts all debt collection against you. However, bankruptcy will almost certainly not be able to discharge your student loan debts unless you can prove they cause you undue hardship. Wage garnishment on student loans occurs when a debtor has defaulted on their student loan payments, and the lender has taken legal action to collect the debt. In this case, the lender can obtain a court order to garnish the debtor's wages. The court will order the debtor's employer to withhold a portion of their paycheck and send it directly to the lender until the debt is paid off. The amount withheld from the debtor's wages can vary depending on state law and the type of loan. Wage garnishment on student loans can have a significant impact on debtors. Losing a portion of their wages can make it difficult for debtors to pay for basic necessities such as rent, food, and utilities. In addition, wage garnishment can damage a debtor's credit score, making it harder to obtain loans or credit in the future. Wage garnishment can also cause emotional distress, as debtors may feel ashamed or embarrassed that they are unable to pay off their student loans. Bankruptcy is a legal process that can help individuals who are unable to pay off their debts. Bankruptcy can provide a fresh start by eliminating certain debts or providing a structured repayment plan. Filing for bankruptcy can also stop wage garnishment on student loans. Bankruptcy is a legal process in which an individual or business seeks relief from their debts. There are two types of bankruptcy available to individuals: Chapter 7 bankruptcy and Chapter 13 bankruptcy. Chapter 7 bankruptcy is also known as liquidation bankruptcy, while Chapter 13 bankruptcy is known as reorganization bankruptcy. Chapter 7 bankruptcy is designed for debtors who have little or no disposable income. In Chapter 7 bankruptcy, a debtor's non-exempt assets are sold to pay off their debts, and any remaining unsecured debts are discharged. Chapter 7 bankruptcy is a relatively quick process, usually lasting only a few months. Chapter 13 bankruptcy is designed for debtors who have a regular income and can afford to make payments towards their debts. In Chapter 13 bankruptcy, the debtor creates a repayment plan that lasts between three and five years. The debtor makes payments to a trustee, who then distributes the payments to their creditors. At the end of the repayment plan, any remaining unsecured debts are discharged. Filing for bankruptcy can stop wage garnishment on student loans. When a debtor files for bankruptcy, an automatic stay is put in place. An automatic stay is a legal order that stops creditors from taking any further action to collect a debt, including wage garnishment. The automatic stay goes into effect immediately upon filing for bankruptcy, and it can provide relief to debtors who are struggling to make ends meet. Bankruptcy can have a significant impact on student loans. Student loans are generally considered non-dischargeable in bankruptcy, meaning they cannot be eliminated through the bankruptcy process. However, there are some exceptions to this rule. In Chapter 7 bankruptcy, student loans are typically not discharged unless the debtor can prove that repaying the loans would cause undue hardship. Undue hardship is a difficult standard to meet, and it typically requires a showing that the debtor cannot maintain a minimal standard of living if forced to repay the loans. This standard is difficult to meet, and most debtors are not successful in having their student loans discharged in Chapter 7 bankruptcy. In Chapter 13 bankruptcy, the debtor creates a repayment plan that includes their student loan payments. The repayment plan lasts between three and five years, during which time the debtor makes payments to a trustee, who then distributes the payments to their creditors. At the end of the repayment plan, any remaining unsecured debts, including student loans, may be discharged. Chapter 7 bankruptcy is designed for debtors who have little or no disposable income. In Chapter 7 bankruptcy, a debtor's non-exempt assets are sold to pay off their debts, and any remaining unsecured debts are discharged. Chapter 7 bankruptcy is a relatively quick process, usually lasting only a few months. Filing for Chapter 7 bankruptcy can stop wage garnishment on student loans. When a debtor files for Chapter 7 bankruptcy, an automatic stay is put in place, which stops creditors, including student loan lenders, from taking any further action to collect a debt, including wage garnishment. The automatic stay can provide debtors with much-needed relief from wage garnishment and other collection efforts. Student loans are generally considered non-dischargeable in Chapter 7 bankruptcy, meaning they cannot be eliminated through the bankruptcy process. However, there are some exceptions to this rule. To have student loans discharged in Chapter 7 bankruptcy, the debtor must prove that repaying the loans would cause undue hardship. As mentioned earlier, this standard is difficult to meet, and most debtors are not successful in having their student loans discharged in Chapter 7 bankruptcy. Chapter 13 bankruptcy is designed for debtors who have a regular income and can afford to make payments towards their debts. In Chapter 13 bankruptcy, the debtor creates a repayment plan that lasts between three and five years. The debtor makes payments to a trustee, who then distributes the payments to their creditors. At the end of the repayment plan, any remaining unsecured debts, including student loans, may be discharged. By filing for Chapter 13 bankruptcy, individuals can also stop the garnishment of their wages due to student loans. This is because when a debtor files for Chapter 13 bankruptcy, an automatic stay is enacted, which prevents creditors (including student loan lenders) from taking any additional measures to collect a debt. The debtor then creates a repayment plan that includes their student loan payments, which must be paid in full during the repayment period. The repayment plan can provide debtors with a structured way to pay off their student loans and can prevent further wage garnishment. In Chapter 13 bankruptcy, the debtor creates a repayment plan that lasts between three and five years. The debtor makes payments to a trustee, who then distributes the payments to their creditors. The repayment plan must include the debtor's student loan payments, which must be paid in full during the repayment period. The repayment plan can provide debtors with a structured way to pay off their student loans and can prevent further wage garnishment. However, it is important to note that the interest on the student loans will continue to accrue during the repayment period. This means that debtors may end up paying more for their student loans than they would have if they had not filed for bankruptcy. To file for bankruptcy, debtors must meet certain requirements. In Chapter 7 bankruptcy, debtors must pass a means test, which compares their income to the median income in their state. If the debtor's income is below the median, they may be eligible for Chapter 7 bankruptcy. If the debtor's income is above the median, they may still be eligible for Chapter 7 bankruptcy if they can show that they have little or no disposable income. In Chapter 13 bankruptcy, debtors must have a regular income and must be able to afford to make payments towards their debts. Debtors must also have less than $419,275 in unsecured debt and less than $1,257,850 in secured debt. Filing for bankruptcy can be a complex process, and it is recommended that debtors seek the advice of a bankruptcy attorney. A bankruptcy attorney can help debtors understand their options, navigate the legal system, and ensure that their rights are protected. A bankruptcy attorney can also help debtors determine whether filing for bankruptcy is the right choice for them and can advise them on the best course of action to take. The timeline for stopping wage garnishment on student loans through bankruptcy can vary depending on the type of bankruptcy and the specific circumstances of the case. In general, the automatic stay goes into effect immediately upon filing for bankruptcy, which means that wage garnishment should stop right away. However, it is important to note that debtors may still owe some money on their student loans even after filing for bankruptcy, and it may take some time to pay off the remaining balance. If you are struggling with wage garnishment on your student loans, there are alternatives to bankruptcy that may help you stop or reduce the amount of your wage garnishment. One alternative to bankruptcy for stopping wage garnishment on student loans is to negotiate a repayment plan with the lender. Many lenders are willing to work with debtors to create a payment plan that is more manageable for them. This can include reducing the monthly payment, extending the repayment period, or temporarily suspending payments. Another alternative is to apply for deferment or forbearance. Deferment and forbearance are both programs that allow debtors to temporarily suspend their payments. Deferment is typically available for certain life events, such as returning to school, while forbearance is usually available for financial hardship. It is important to note that interest may still accrue during the deferment or forbearance period, which means that debtors may end up paying more for their loans in the long run. A third alternative to bankruptcy for stopping wage garnishment on student loans is to consolidate or rehabilitate the loans. Loan consolidation involves combining multiple loans into one loan with a single monthly payment, while loan rehabilitation involves making a series of on-time payments to bring the loans out of default. Both options can help debtors get their loans back on track and may prevent wage garnishment. Wage garnishment on student loans can be a significant burden for debtors who are already struggling to make ends meet. However, filing for bankruptcy can provide a solution for those who are facing wage garnishment on their student loans. Both Chapter 7 and Chapter 13 bankruptcy can stop wage garnishment on student loans, although student loans are generally considered non-dischargeable in bankruptcy, with few exceptions. Debtors who are considering filing for bankruptcy to stop wage garnishment on student loans should be aware of the requirements and steps involved in the process, as well as the role of a bankruptcy attorney in helping them navigate the legal system. It is also important for debtors to consider alternatives to bankruptcy, such as negotiating a repayment plan with their lender, applying for deferment or forbearance, or consolidating or rehabilitating their loans. Ultimately, the decision to file for bankruptcy to stop wage garnishment on student loans should not be taken lightly. Debtors should seek the advice of a professional and carefully consider their options before making a decision. Filing for bankruptcy can have a significant impact on a debtor's credit score and financial future, and it is important to weigh the benefits and drawbacks before moving forward. However, for those who are struggling with wage garnishment on their student loans, bankruptcy can provide much-needed relief and a fresh start towards a debt-free future.Can Filing Bankruptcy Stop Wage Garnishment on Student Loans?

Definition of Wage Garnishment on Student Loans

The Impact of Wage Garnishment on Debtors

Bankruptcy and Wage Garnishment

The Basics of Bankruptcy and Its Types

How Bankruptcy Can Stop Wage Garnishment

The Effect of Bankruptcy on Student Loans

Chapter 7 Bankruptcy and Wage Garnishment on Student Loans

How Chapter 7 Bankruptcy Can Stop Wage Garnishment on Student Loans

The Dischargeability of Student Loans in Chapter 7 Bankruptcy

Chapter 13 Bankruptcy and Wage Garnishment on Student Loans

How Chapter 13 Bankruptcy Can Stop Wage Garnishment on Student Loans

The Repayment Plan in Chapter 13 Bankruptcy and Its Impact on Student Loans

The Process of Filing for Bankruptcy to Stop Wage Garnishment on Student Loans

Requirements and Steps Involved in Filing for Bankruptcy

Role of a Bankruptcy Attorney in the Process

Timeline for Stopping Wage Garnishment on Student Loans Through Bankruptcy

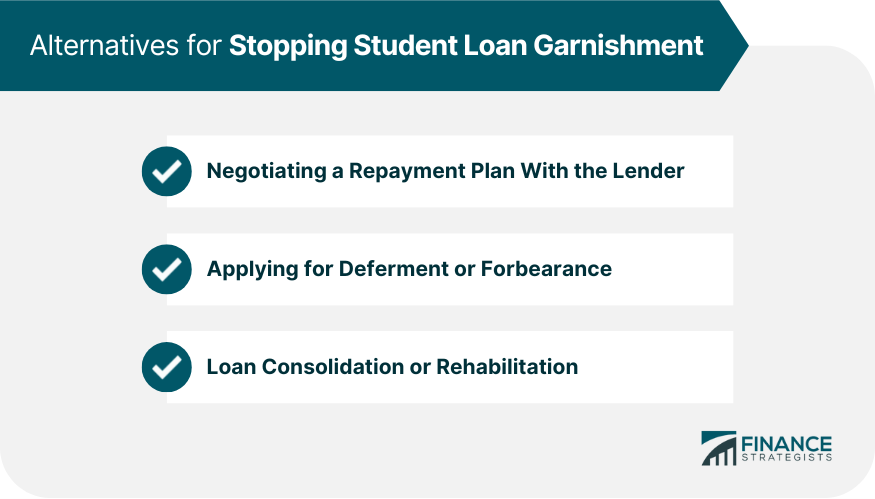

Alternatives to Bankruptcy for Stopping Wage Garnishment on Student Loans

Negotiating a Repayment Plan With the Lender

Applying for Deferment or Forbearance

Loan Consolidation or Rehabilitation

Conclusion

Can Filing Bankruptcy Stop Wage Garnishment on Student Loans? FAQs

Filing for bankruptcy puts an automatic stay in place, which stops creditors, including student loan lenders, from taking further action to collect a debt, including wage garnishment.

Student loans are generally considered non-dischargeable in bankruptcy, but they may be discharged if the debtor can prove that repaying the loans would cause undue hardship.

The requirements for filing for bankruptcy vary depending on the type of bankruptcy. In Chapter 7 bankruptcy, debtors must pass a means test, while in Chapter 13 bankruptcy, debtors must have a regular income and be able to make payments towards their debts.

No, there are other options for stopping wage garnishment on student loans, such as negotiating a repayment plan with the lender, applying for deferment or forbearance, or consolidating or rehabilitating the loans.

A bankruptcy attorney can help debtors understand their options, navigate the legal system, and ensure that their rights are protected. They can also advise debtors on the best course of action to take and can help with the bankruptcy filing process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.