Pension buyouts are financial transactions in which a company or pension plan sponsor transfers some or all of its pension obligations to an insurance company or provides a lump-sum payment to plan participants. This process allows the sponsor to reduce or eliminate its pension liabilities, mitigate risk, and streamline its balance sheet. Pension buyouts are attractive to companies for various reasons, including reducing the volatility and financial risk associated with managing a pension plan. By transferring the pension obligations to an insurer or offering lump-sum payments, companies can free up resources and focus on their core business operations. Additionally, pension buyouts can improve a company's financial position and reduce regulatory and compliance burdens. Pension plan sponsors are typically employers or organizations that offer pension benefits to their employees or members. They are responsible for managing the pension plan, making contributions, and ensuring the plan's financial stability. Plan sponsors initiate pension buyouts to manage their pension liabilities. Insurance companies play a critical role in pension buyouts by providing annuity contracts that guarantee lifetime income to plan participants. In an annuity purchase, the insurance company assumes the responsibility for making future pension payments and managing the associated risks. Financial advisors help pension plan sponsors navigate the complexities of pension buyouts by providing guidance on the financial, legal, and regulatory aspects of the process. They also assist in evaluating the costs and benefits of the buyout and selecting the best option for the plan sponsor and participants. Plan participants are the employees or members of an organization who are entitled to pension benefits. Beneficiaries are the individuals designated to receive pension benefits in case of a participant's death. Both participants and beneficiaries can be affected by pension buyouts, as they may experience changes in their benefits, financial security, and retirement planning. The funding status of a pension plan is a critical factor in determining the feasibility and cost of a pension buyout. A well-funded plan with sufficient assets to cover its liabilities is more likely to be able to afford a buyout, while an underfunded plan may require additional contributions or face challenges in executing a buyout. Pension buyouts can be expensive, as they involve paying a premium to the insurance company or offering lump-sum payments to plan participants. Plan sponsors must carefully assess the cost of the buyout and compare it to the potential benefits and savings. Interest rates and market conditions can significantly impact the cost and timing of pension buyouts. Low-interest rates can increase the cost of annuity purchases, while favorable market conditions can improve the funding status of the pension plan, making a buyout more feasible. Longevity risk refers to the uncertainty surrounding the life expectancy of plan participants, which can impact the cost of pension liabilities. Pension buyouts can help plan sponsors transfer the longevity risk to insurance companies or eliminate it through lump-sum payments. Pension buyouts are subject to various legal and regulatory requirements, including disclosure and communication rules, fiduciary responsibilities, and protections for plan participants. Plan sponsors must navigate these requirements carefully to ensure a successful buyout process. Lump-sum buyouts offer several advantages, such as providing plan participants with immediate access to their pension benefits, which can be invested or used to meet financial needs. However, they also carry risks, as participants may not have the financial expertise to manage their retirement savings effectively and may outlive their lump-sum payment. Not all plan participants may be eligible for a lump-sum buyout, as eligibility criteria can vary depending on the plan's provisions and the plan sponsor's objectives. Typically, lump-sum buyouts are offered to vested participants who have terminated their employment or are close to retirement. Lump-sum payments are subject to federal tax and state taxes, which can significantly impact the net amount received by plan participants. Participants may also face penalties if they withdraw the funds before reaching the age of 59½. Group annuity contracts are insurance products that provide a stream of income to plan participants in exchange for transferring the pension obligations to the insurance company. These contracts guarantee lifetime income and offer protection against longevity risk. Annuity purchases offer several benefits, including the transfer of pension liabilities and risks to the insurance company, guaranteed income for plan participants, and protection against longevity risk. However, they can also be expensive and may result in reduced benefits for some participants, depending on the terms of the annuity contract. Transferring pension obligations to an insurance company involves several steps, including selecting an insurer, negotiating the terms of the annuity contract, and transferring the plan assets to the insurance company. Plan sponsors must also communicate the changes to the plan participants and provide them with information about their new annuity benefits. Annuity purchases are subject to regulatory oversight by state insurance departments and federal agencies, such as the Department of Labor and the Pension Benefit Guaranty Corporation (PBGC). These agencies ensure that insurance companies meet their financial obligations and that plan participants' rights and benefits are protected. Pension buyouts can have a significant impact on plan participants' financial security and retirement planning. Lump-sum payments may provide immediate access to funds, but participants must carefully manage their investments to ensure they have adequate retirement income. Annuity purchases guarantee lifetime income but may result in reduced benefits for some participants. Pension buyouts can result in changes to plan participants' benefits, such as the elimination or reduction of cost-of-living adjustments, early retirement subsidies, or survivor benefits. Plan sponsors must clearly communicate these changes and provide participants with information about their new benefits. Pension buyouts can expose plan participants to various risks, including investment risk in the case of lump-sum payments and the financial stability of the insurance company in the case of annuity purchases. Regulatory agencies and legal protections help mitigate these risks and safeguard participants' benefits. Plan sponsors are required to provide plan participants with timely and accurate information about the pension buyout process, the changes to their benefits, and their rights and protections under the law. Effective communication is essential to ensure that participants understand the implications of the buyout and can make informed decisions about their retirement planning. A pension freeze is a strategy in which a plan sponsor stops accruing new pension benefits for some or all participants. This approach can help control pension costs and liabilities without transferring the obligations to an insurance company or offering lump-sum payments. Pension plan mergers involve combining two or more pension plans into a single plan, which can streamline plan administration, reduce costs, and improve the funding status of the combined plan. This strategy can be an alternative to pension buyouts for companies with multiple pension plans or those seeking to consolidate their pension liabilities. Plan termination involves the complete shutdown of a pension plan, with the plan sponsor paying out all accrued benefits to plan participants, either through lump-sum payments or annuity purchases. This approach eliminates the plan sponsor's pension obligations but can be costly and disruptive for plan participants. LDI strategies involve managing a pension plan's investments to match its liabilities more closely, reducing the plan's exposure to interest rate and market risks. By implementing an LDI strategy, plan sponsors can improve the plan's funding status and mitigate the need for a pension buyout. Pension buyouts are complex financial transactions that involve transferring pension obligations to an insurance company or offering lump-sum payments to plan participants. These transactions can help plan sponsors manage their pension liabilities, reduce risk, and improve their financial position. However, they also carry potential risks and challenges for plan participants, who may experience changes in their benefits and financial security. Pension buyouts play a crucial role in the retirement planning landscape, as they can significantly impact the financial security and retirement income of plan participants. Plan sponsors, insurance companies, and regulators must carefully navigate the pension buyout process to ensure that the interests of all stakeholders are protected. To ensure a successful pension buyout, plan sponsors should carefully evaluate the costs and benefits of the transaction, consider alternative strategies, engage experienced financial advisors, and maintain open and transparent communication with plan participants. Insurance companies should provide competitive annuity products that offer adequate protection and income for plan participants. Regulators should enforce disclosure and communication requirements and monitor the financial stability of insurance companies to protect plan participants' rights and benefits.What Are Pension Buyouts?

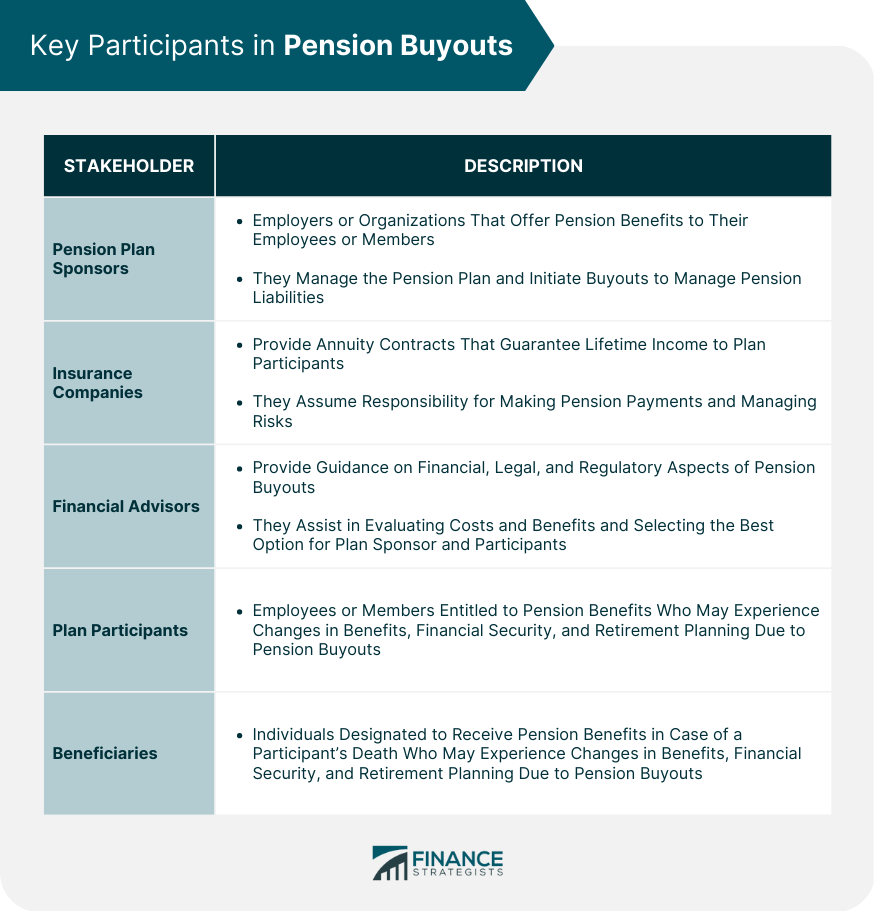

Key Participants in Pension Buyouts

Pension Plan Sponsors

Insurance Companies

Financial Advisors

Plan Participants and Beneficiaries

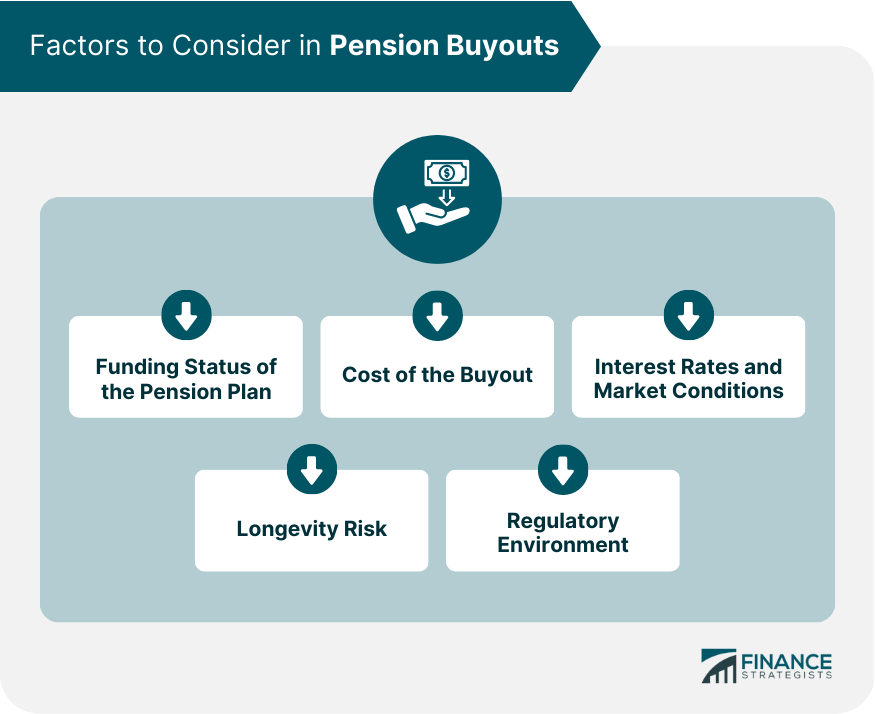

Factors to Consider in Pension Buyouts

Funding Status of the Pension Plan

Cost of the Buyout

Interest Rates and Market Conditions

Longevity Risk

Regulatory Environment

Types of Pension Buyouts

Lump-Sum Buyouts

Advantages and Disadvantages

Eligibility Criteria

Tax Implications

Annuity Purchases

Group Annuity Contracts

Benefits and Drawbacks

Process for Transferring Pension Obligations

Regulatory Oversight

Impact of Pension Buyouts on Plan Participants

Financial Security and Retirement Planning

Change in Benefits

Risks and Protections

Communication and Disclosure Requirements

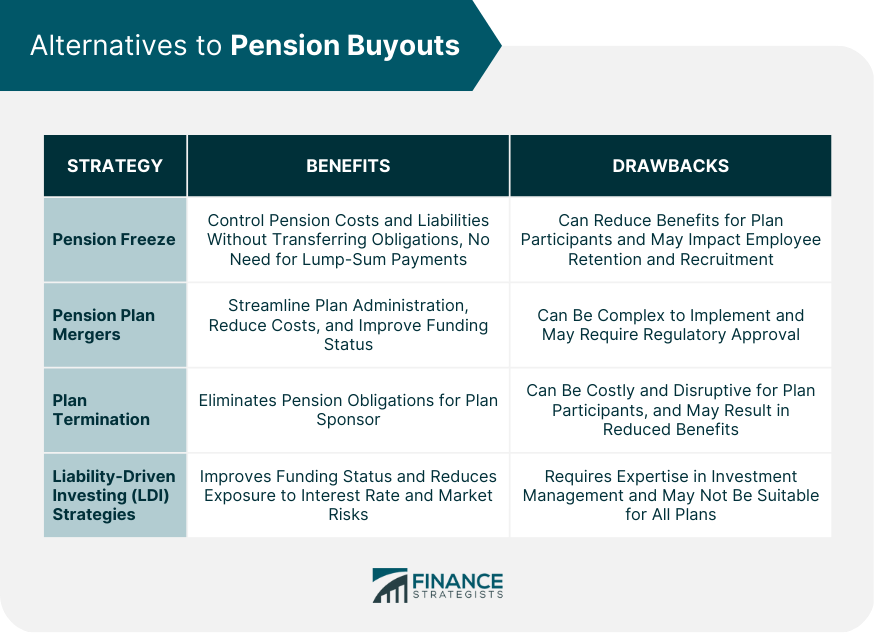

Alternatives to Pension Buyouts

Pension Freezes

Pension Plan Mergers

Plan Termination

Liability-Driven Investing (LDI) Strategies

Conclusion

Pension Buyouts FAQs

A pension buyout is a transaction in which a company offers a lump sum payment to a retiree in exchange for giving up their monthly pension payment.

Companies offer pension buyouts to reduce their long-term pension obligations and risk. By offering a lump sum payment, they can transfer the pension obligation to the retiree and eliminate the ongoing pension payment.

It depends on your individual circumstances. If you need a lump sum of money for immediate expenses or investments, a pension buyout may be a good option. However, if you value the security of a guaranteed monthly pension payment, you may want to decline the buyout.

If you accept a buyout, you will receive a lump sum payment in exchange for giving up your monthly pension payment. The lump sum payment may be less than the total value of your pension, so it's important to carefully consider the offer before accepting.

It may be possible to negotiate the terms of a pension buyout, such as the amount of the lump sum payment or the timing of the payment. However, it's important to understand the terms of the original pension plan and the implications of any changes before entering into negotiations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.