Retirement is often framed as a single moment—the day you stop working. In reality, it’s better understood as a transition from required work to optional work. Traditionally, retirement meant leaving the workforce entirely after decades of full-time employment. That definition still applies for some, but it no longer reflects how most people approach this stage of life. Today, retirement is less about stopping and more about changing how and why you work. For some, it means stepping away completely and living off savings, Social Security, or pensions. For others, it means shifting into part-time roles, consulting, or passion-driven projects that provide both income and purpose. The common thread is choice—work becomes something you can do, not something you have to do. This shift matters because it reframes the entire conversation. Instead of asking, “When do I stop working?”, a better question is, “When do I have the financial freedom to decide how I spend my time?” Retirement, at its core, isn’t defined by age. It’s defined by independence, flexibility, and control. The short answer is no. There is no legal requirement in the United States forcing you to retire at a specific age. You can continue working as long as you want, as long as you’re able and your employer allows it. What most people call “retirement age” is often confused with Social Security full retirement age (FRA). This is simply the age at which you’re eligible to receive your full Social Security benefit without reduction. Depending on your birth year, that typically falls between 66 and 67. But here’s the key distinction: that age determines your benefits—not your employment status. You are free to retire earlier than your full retirement age if you have the financial means to support yourself. You can also continue working well beyond it, either by choice or necessity. Some people begin collecting Social Security benefits while still employed, while others delay claiming benefits in order to increase their monthly income later on. None of these decisions are restricted by a mandatory retirement rule. There is no point at which the government or the system forces you to stop working. Retirement is not dictated by law—it is a personal decision shaped by your finances, your goals, and your readiness. That said, while you don’t have to retire at a certain age, the timing of your decision still carries financial consequences. And that’s where the real planning begins. If you begin claiming benefits at age 62, rather than waiting until your full retirement age, your monthly benefit can be reduced by as much as 25% to 30%, depending on your birth year. This reduction isn’t temporary—it lasts for the rest of your life. Over time, that smaller monthly check can add up to a significant difference in total lifetime income, particularly if you live into your 80s or 90s. It also reduces the baseline income you can rely on during retirement, which may increase your dependence on other assets. For some, claiming early still makes sense, especially if there are health concerns or a need for immediate income. But it’s a decision that should be made with a clear understanding of the long-term implications. Retiring early means you’re asking your savings to do more—and to do it for longer. Without full Social Security benefits, and with fewer years of earned income, your retirement accounts become the primary source of support. This increases the pressure on your portfolio and raises the risk of depleting your assets too quickly, especially during market downturns. There’s also the issue of sequence of returns risk. If you begin withdrawing from your investments during a market decline, early losses can have an outsized impact on the longevity of your portfolio. Over a 25- to 30-year retirement, even small miscalculations can compound into larger shortfalls. Because of this, early retirees often need a more conservative and well-structured withdrawal strategy. This may include maintaining larger cash reserves, diversifying income sources, and adjusting spending dynamically based on market conditions. Healthcare is one of the most significant—and often underestimated—challenges of early retirement. Medicare eligibility does not begin until age 65. If you retire before then, you’ll need to secure coverage through alternative means, such as COBRA continuation coverage, private marketplace plans, or a spouse’s employer-sponsored insurance. These options can be expensive, particularly for individuals who no longer have employer subsidies. Premiums, deductibles, and out-of-pocket costs can quickly become a major expense, especially if unexpected medical issues arise. Beyond the cost, there’s also the complexity of navigating coverage options, ensuring continuity of care, and managing potential gaps. For many early retirees, healthcare becomes one of the defining factors in whether their plan is sustainable. One of the primary advantages of retiring at full retirement age is that you’re eligible to receive 100% of your Social Security benefit, based on your earnings history. Unlike early retirement, there are no permanent reductions applied to your monthly payments. This provides a stable and predictable income stream that can serve as a foundation for your retirement plan. For many individuals, Social Security becomes a core component of their cash flow, helping cover essential expenses such as housing, food, and utilities. Additionally, reaching full retirement age eliminates the earnings limits that apply to those who claim benefits earlier. This means that if you choose to continue working in any capacity, your benefits will not be reduced due to income. That added flexibility can be valuable, especially for those transitioning gradually out of the workforce. By working through your early and mid-60s, you give your retirement savings more time to grow—both through continued contributions and potential market appreciation. Even a few additional years of saving and compounding can have a meaningful impact on your overall financial position. You’re not only increasing the size of your portfolio, but also reducing the number of years those funds will need to support you. This combination can significantly improve the sustainability of your retirement plan. There’s also a psychological benefit here. Retiring at full retirement age often provides a greater sense of financial confidence, as you’ve had more time to prepare and can enter retirement with a clearer understanding of your income sources and expenses. Another advantage of retiring around full retirement age is the alignment with Medicare eligibility, which begins at age 65. By this point, most individuals either already have Medicare coverage or are transitioning into it, which simplifies one of the more complex aspects of retirement planning. Compared to retiring earlier, you’re less likely to face a prolonged period of high, unsubsidized healthcare costs. This alignment reduces uncertainty and allows for more predictable budgeting when it comes to medical expenses. It also makes it easier to coordinate supplemental insurance, prescription drug plans, and long-term care considerations. Retiring at full retirement age often represents a middle ground between maximizing financial outcomes and enjoying retirement sooner rather than later. You avoid the steep benefit reductions associated with early retirement, while still leaving room to enjoy your time before advancing too far into later stages of life. For many, this timing strikes a balance between practicality and lifestyle—offering enough financial security without delaying retirement indefinitely. At the same time, it allows for flexibility. Some individuals choose to fully retire at this point, while others scale back into part-time or advisory roles. The key advantage is that you’re making the decision from a position of greater stability. For each year you postpone claiming benefits beyond your full retirement age, your monthly payment increases through delayed retirement credits. In practical terms, this can result in a substantially higher guaranteed income for the rest of your life. That increase is especially valuable because Social Security is one of the few income sources that is adjusted for inflation and continues for as long as you live. A higher monthly benefit can also provide greater financial security later in retirement, particularly in your 80s and 90s, when other assets may be declining. For individuals concerned about longevity risk, delaying benefits can act as a form of built-in protection. Continuing to work allows you to postpone withdrawals from your retirement accounts, which can have a powerful impact on the longevity of your portfolio. Instead of drawing down your assets, you give them more time to grow. At the same time, you shorten the number of years those funds will need to support you. This dual effect—continued compounding combined with fewer withdrawal years—can significantly improve the sustainability of your retirement plan. It also reduces exposure to sequence of returns risk. By delaying withdrawals, you’re less likely to be forced to sell investments during a market downturn early in retirement, which can preserve the long-term value of your portfolio. Working beyond full retirement age provides ongoing earned income, which can support your lifestyle without relying heavily on savings. In some cases, it also allows you to maintain access to employer-sponsored benefits, such as health insurance, retirement contributions, or other perks that would otherwise need to be replaced at your own expense. Additionally, continued earnings may increase your Social Security benefit if they replace lower-earning years in your calculation history. While the impact varies, it can provide a modest boost to your overall benefit. Financial benefits aside, many people choose to delay retirement because they enjoy working or value the structure it provides. Work can offer a sense of identity, routine, and social connection that’s difficult to replicate in retirement. For some, stepping away entirely can feel abrupt or even disorienting. Continuing to work—whether full-time or in a reduced capacity—can create a smoother transition. However, this is also where tradeoffs come into play. Delaying retirement means postponing the full freedom that retirement offers. Health, energy levels, and personal priorities all factor into whether extending your career is the right choice. At the foundation of any retirement decision is financial readiness. This goes beyond simply having savings—it’s about understanding whether your income streams can reliably support your lifestyle over time. That includes evaluating Social Security, retirement accounts, pensions (if applicable), and any additional income sources. The key question is whether these sources, combined, can cover both essential expenses and discretionary spending without creating unnecessary risk. Consistency matters just as much as the total amount. A plan built on stable, predictable income is far more resilient than one dependent on variable withdrawals or market performance alone. Retirement isn’t just a financial shift—it’s a lifestyle change. Your expenses will likely evolve, not disappear. Some costs may decrease, such as commuting or work-related expenses. Others may increase, particularly in areas like travel, hobbies, or healthcare. Housing decisions—whether downsizing, relocating, or staying put—also play a significant role. The clearer you are about how you want to spend your time, the easier it becomes to estimate what that lifestyle will cost. A vague retirement vision often leads to vague financial planning, which can create unnecessary uncertainty. With increasing life expectancies, it’s not uncommon for retirement to span 25 to 30 years or more. That extended time horizon places greater pressure on your savings and requires a plan that can adapt to changing conditions over decades. Planning conservatively—assuming a longer lifespan—helps reduce the risk of outliving your assets. It also encourages more thoughtful decisions around withdrawal rates, asset allocation, and guaranteed income sources. Healthcare is one of the most unpredictable—and potentially expensive—components of retirement. Your timing decision should account for when you’ll become eligible for Medicare and how you’ll cover costs before and after that transition. Premiums, out-of-pocket expenses, and long-term care considerations all need to be factored into your plan. Even for those with solid savings, healthcare costs can significantly impact retirement sustainability. Addressing this early can prevent unexpected financial strain later. Retirement doesn’t have to be an all-or-nothing decision. Many people benefit from maintaining some level of flexibility in how they transition out of full-time work. This could mean shifting to part-time roles, consulting, or pursuing income-generating hobbies. Having the option to earn—even modestly—can reduce pressure on your savings and provide an added layer of financial security. Flexibility also allows you to adjust your plan if circumstances change, whether due to market conditions, personal preferences, or unexpected expenses. While financial readiness is critical, it’s only part of the equation. Retirement also represents a significant psychological shift. Work often provides structure, identity, and social interaction. Removing that abruptly can lead to a sense of loss or uncertainty, especially if there’s no clear plan for how to fill that time. Being intentional about how you’ll spend your days—whether through travel, family, hobbies, or new pursuits—can make the transition smoother and more fulfilling. The timing of your retirement can also influence your tax situation in meaningful ways. Decisions around when to withdraw from retirement accounts, when to claim Social Security, and how to manage taxable income can all affect your overall tax liability. In some cases, working an extra year or delaying withdrawals can create opportunities for more efficient tax planning. Coordinating these elements helps ensure that you’re not only generating income, but doing so in a way that preserves more of it over time. Retirement isn’t a fixed age or a mandated endpoint—it’s a personal decision shaped by your financial readiness, lifestyle goals, and sense of purpose. While traditional benchmarks like full retirement age provide useful guidelines, they don’t define when you should step away from work. What matters most is whether you have the flexibility and resources to make work optional. Every path—retiring early, on time, or later—comes with tradeoffs. The right choice depends on how those tradeoffs align with your priorities, from income stability to how you want to spend your time. Because of the financial complexity involved, it’s often wise to consult a qualified financial advisor who can help you evaluate your options, optimize your strategy, and avoid costly missteps. In the end, retirement isn’t about reaching a certain age—it’s about reaching a point where you have control over what comes next.Definition of Retirement

Do You Have to Retire at Retirement Age?

Financial Implications of Retiring Early (Before FRA)

Reduced Social Security Benefits

Greater Reliance on Savings

Healthcare Coverage Gap

Financial Implications of Retiring at FRA

Full Access to Social Security Benefits

More Time to Build and Strengthen Savings

Alignment With Medicare and Healthcare Planning

A Balanced Approach to Risk and Lifestyle

Financial Implications of Delaying Retirement

Higher Monthly Social Security Income

Reduced Pressure on Retirement Savings

Continued Income and Potential Benefits

Lifestyle and Purpose Considerations

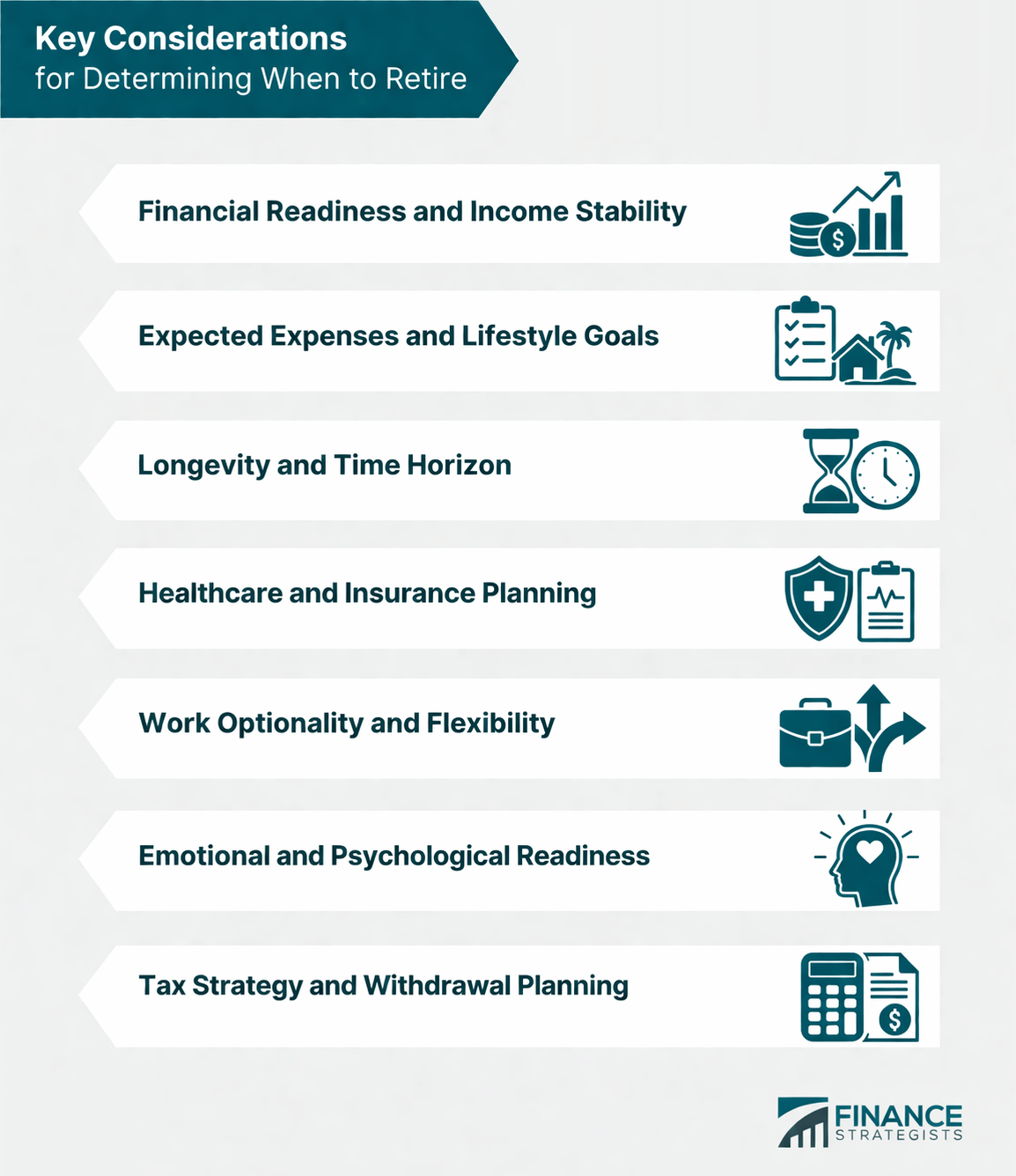

Key Considerations for Determining When to Retire

Financial Readiness and Income Stability

Expected Expenses and Lifestyle Goals

Longevity and Time Horizon

Healthcare and Insurance Planning

Work Optionality and Flexibility

Emotional and Psychological Readiness

Tax Strategy and Withdrawal Planning

Final Thoughts

Do You Have to Retire at Retirement Age? FAQs

No. There is no legal requirement to retire at a specific age in the United States. You can continue working as long as you choose and are able.

Full retirement age is the age at which you can receive 100% of your Social Security benefits, typically between 66 and 67 depending on your birth year.

No. Many people transition into part-time work, consulting, or passion projects while still considering themselves retired.

It depends on your financial situation, health, and goals. Retiring early offers more time freedom, while delaying can increase your Social Security benefits and strengthen your savings.

You can retire at any age if you have the financial means, but Social Security benefits can typically begin at age 62 with reduced payments.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.