Hard money lending is a form of short-term, asset-based financing where private individuals or companies provide loans to borrowers, primarily secured by real estate. These loans are commonly used for real estate investments, development projects, or property flips when traditional financing is not available or not suitable. While traditional lending relies on a borrower's creditworthiness, income, and financial history, hard money lending focuses on the value of the underlying asset or property. Hard money loans generally have higher interest rates, shorter loan terms, and faster funding times compared to traditional loans. Hard money lending offers several advantages, such as quick access to funds, flexible terms, and less stringent qualification requirements. However, it also has disadvantages, including higher interest rates, shorter repayment periods, and the risk of losing the collateral in case of default. Private individuals, also known as private money lenders or private investors, provide hard money loans using their personal funds. They often have a high net worth and are seeking alternative investment opportunities. Private companies, such as hedge funds and private equity firms, also engage in hard money lending. These companies pool investor funds to provide loans to borrowers. Real estate investors often use hard money loans to acquire, renovate, or develop properties for resale or rental purposes. Developers may use hard money loans to finance the construction or development of residential or commercial projects. Home flippers use hard money loans to purchase, renovate, and quickly sell properties for profit. Brokers connect borrowers with hard money lenders, often assisting in loan negotiation and origination. Consultants provide advice and guidance to borrowers and lenders in navigating the hard money lending process. Bridge loans are short-term loans used to finance a property or project until permanent financing or the next stage of financing becomes available. Fix-and-flip loans are designed for borrowers who intend to purchase, renovate, and quickly sell a property for profit. Construction loans provide financing for the development or renovation of residential or commercial projects. Land loans are used to finance the acquisition and development of raw or undeveloped land. Other asset-based loans include loans secured by assets other than real estate, such as equipment, vehicles, or inventory. LTV is the ratio of the loan amount to the value of the property. Hard money lenders typically lend up to 65-75% of the property's value. ARV is the estimated value of the property after repairs and improvements are completed. Lenders often lend up to 70% of the ARV. While hard money lenders focus on the asset's value, they may still consider the borrower's credit score, income, and experience in real estate investing. Hard money loans are secured by real estate or other valuable assets. In case of default, the lender can seize and sell the collateral to recover their investment. The hard money loan application process typically includes the submission of a loan application, appraisal of the property, underwriting, and closing. This process is generally faster than traditional loan application processes. Interest rates for hard money loans depend on several factors, including the lender's risk assessment, loan term, property location, and the borrower's experience and creditworthiness. Hard money loans generally have higher interest rates than traditional loans, ranging from 9% to 15% or higher. Hard money lenders often charge loan origination fees, which can range from 1% to 3% of the loan amount. Other fees may include appraisal fees, document preparation fees, and closing costs. Borrowers face high-interest rates and fees, which can significantly impact their profitability and cash flow. Short loan terms may create pressure on borrowers to complete projects and repay the loan quickly, leading to potential financial strain. If a borrower defaults on a hard money loan, they risk losing their collateral, which is often the underlying property. Lenders face the risk of borrowers defaulting on their loans, which may result in a loss of investment and the need to manage the foreclosure process. Hard money lenders are exposed to market risk, as fluctuations in real estate values and demand can impact the value of the collateral and the borrower's ability to repay the loan. Lenders must navigate a complex regulatory environment, ensuring compliance with federal and state laws and regulations. Federal regulations affecting hard money lending include the Truth in Lending Act (TILA), the Real Estate Settlement Procedures Act (RESPA), and the Dodd-Frank Wall Street Reform and Consumer Protection Act. State regulations for hard money lending vary and may include licensing requirements, interest rate caps, and disclosure requirements. Lenders must comply with applicable federal and state laws and regulations, including those governing loan terms, disclosure, and licensing. Online lending platforms streamlines the hard money lending process, providing borrowers with easier access to lenders and faster loan approvals. Automation and artificial intelligence (AI) can improve the efficiency and accuracy of underwriting, risk assessment, and loan processing. The hard money lending market is expected to grow due to increased demand for alternative financing options, particularly in the real estate sector. Hard money lenders face challenges, such as increased competition, regulatory changes, and market fluctuations. However, they also have opportunities to expand their services, adopt new technologies, and tap into new markets. Hard money lending serves as a vital alternative financing option, particularly in the real estate sector. It offers several advantages, such as quick access to funds, flexible terms, and a focus on the asset's value rather than creditworthiness. However, it also comes with inherent risks and challenges for both borrowers and lenders, including higher interest rates, shorter loan terms, and potential loss of collateral. Given the complexities and risks involved in hard money lending, it is crucial for borrowers and lenders to carefully consider their options and navigate the process with diligence. Partnering with an experienced mortgage broker can be an invaluable asset, as they can connect borrowers with suitable hard money lenders, assist in loan negotiation and origination, and provide expert guidance throughout the process. What Is Hard Money Lending?

Differences Between Hard Money Lending and Traditional Lending

Advantages and Disadvantages of Hard Money Lending

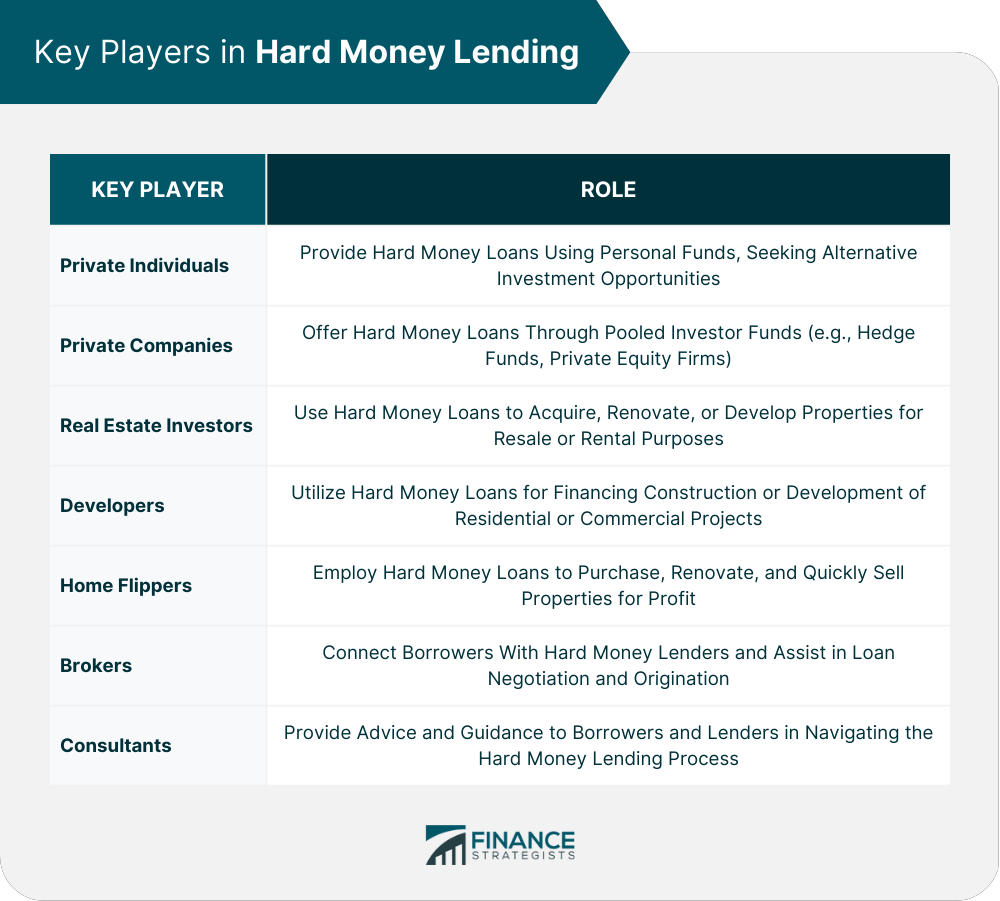

Key Players in Hard Money Lending

Hard Money Lenders

Private individuals

Private companies

Borrowers

Real estate investors

Developers

Home flippers

Intermediaries

Brokers

Consultants

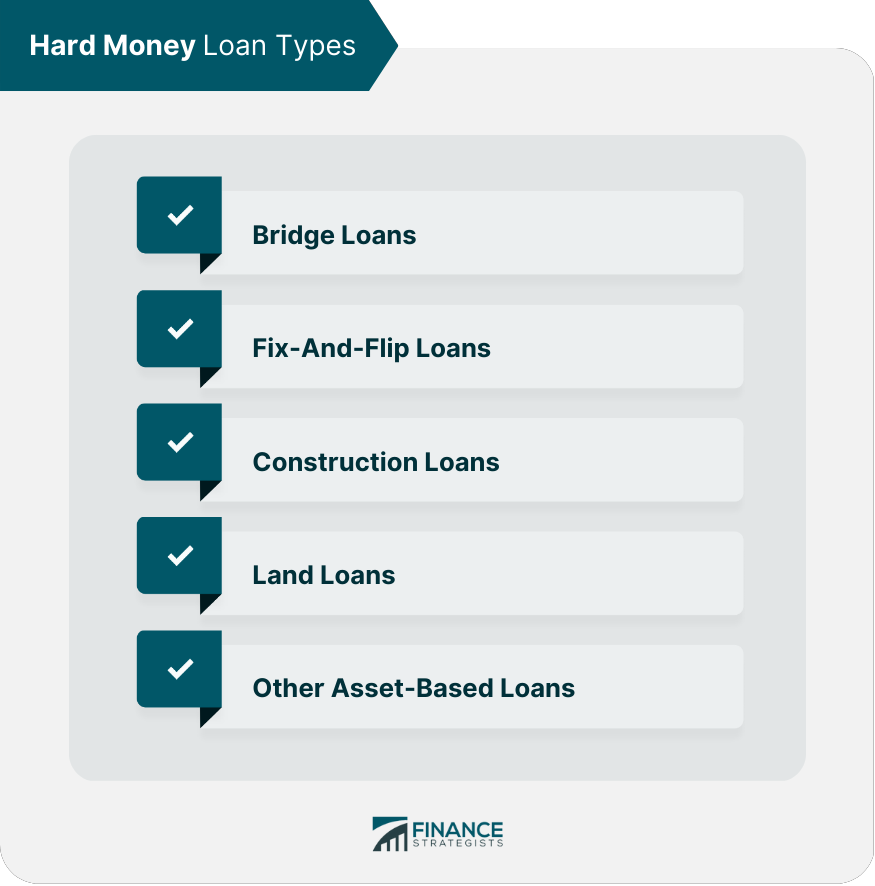

Hard Money Loan Types

Bridge Loans

Fix-And-Flip Loans

Construction Loans

Land Loans

Other Asset-Based Loans

Qualification Criteria and Loan Process

Loan-To-Value (LTV) Ratio

After-Repair-Value (ARV) Ratio

Creditworthiness and Experience

Collateral

Loan Application Process

Interest Rates and Fees

Factors Affecting Interest Rates

Typical Interest Rates

Loan Origination and Other Fees

Risks and Challenges of Hard Money Lending

Risk for Borrowers

High-Interest Rates and Fees

Short Loan Terms

Loss of Collateral

Risk for Lenders

Default Risk

Market Risk

Regulatory Risk

Regulation and Compliance

Federal Regulations

State Regulations

Compliance Requirements for Lenders

Future of Hard Money Lending

Technological Advancements

Online Lending Platforms

Automation and AI

Market Growth and Trends

Challenges and Opportunities

The Bottom Line

Hard Money Lending FAQs

Hard money lending is a form of short-term, asset-based financing where private individuals or companies provide loans primarily secured by real estate. Unlike traditional lending, which relies on creditworthiness and financial history, hard money lending focuses on the value of the underlying asset. It usually has higher interest rates, shorter loan terms, and faster funding times compared to traditional loans.

Borrowers in hard money lending are usually real estate investors, developers, and home flippers. They seek hard money loans for various purposes, such as property acquisitions, renovations, development projects, or short-term financing needs when traditional financing is not suitable or available.

Hard money lending offers various loan types, including bridge loans, fix-and-flip loans, construction loans, land loans, and other asset-based loans. Each loan type is designed to cater to specific needs and purposes in real estate financing.

Interest rates for hard money loans are typically higher than traditional loans, ranging from 9% to 15% or higher, depending on factors such as risk assessment, loan term, property location, and borrower's creditworthiness. Hard money lenders may also charge loan origination fees, appraisal fees, document preparation fees, and closing costs.

Yes, hard money lending involves risks and challenges for both borrowers and lenders. Borrowers face high interest rates, short loan terms, and the risk of losing collateral in case of default. Lenders, on the other hand, face default risk, market risk, and regulatory risk. It is crucial for both parties to carefully consider the risks and benefits involved in hard money lending and work with experienced professionals, such as mortgage brokers, to navigate the process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.