Disability insurance is a type of insurance that provides income replacement or financial support to individuals who become disabled and are unable to work due to an injury or illness. Disability insurance can be purchased by individuals or provided by employers as part of a benefits package. Disability insurance policies typically provide benefits that replace a portion of the individual's income while they are disabled, and may also cover medical expenses and rehabilitation costs. Disability insurance can provide financial security and peace of mind for individuals and families in the event of a disability. Consider the following types: Short-term disability insurance provides temporary income replacement for individuals who are unable to work due to a non-work-related illness or injury. The coverage period typically ranges from a few weeks to a few months. Long-term disability insurance provides income replacement for an extended period, usually lasting several years or until the policyholder reaches retirement age. This type of insurance is essential for individuals who face the possibility of long-term health issues or permanent disability. Social Security disability insurance (SSDI) is a government-sponsored program that provides income replacement for eligible workers who have become disabled and can no longer work. Benefits are based on the individual's earnings record and work history. Business overhead expense insurance is designed for business owners who want to protect their business from the financial impact of their disability. This type of insurance covers the ongoing expenses of running a business, such as rent, utilities, and employee salaries. A residual disability rider provides partial income replacement if you can still work but are unable to perform all your job duties or work full-time due to disability. This rider is essential for individuals who may be able to continue working in a limited capacity. The benefits paid under a residual disability rider are typically calculated as a percentage of the total disability benefit, based on the reduction in your income or working hours. A COLA rider adjusts your disability benefits annually to account for inflation, ensuring that your purchasing power remains consistent over time. This rider is particularly important for long-term disability policies, as the value of your benefits may erode over time due to inflation. The COLA rider typically uses a standard measure of inflation, such as the Consumer Price Index, to determine the annual adjustment. The benefit increase is usually capped at a specific percentage per year. An FIO rider allows you to increase your disability coverage in the future without undergoing additional underwriting or providing proof of insurability. This rider is useful for individuals who expect their income to rise over time and want to ensure adequate coverage. The FIO rider generally allows for scheduled increases in coverage, either at specific intervals or upon the occurrence of certain life events, such as a promotion or marriage. A catastrophic disability rider provides an additional benefit in the event of a severe disability, such as the loss of multiple limbs or severe cognitive impairment. This rider is designed to help cover the increased costs associated with catastrophic disabilities. The catastrophic disability rider typically pays a lump sum or an additional monthly benefit, depending on the policy terms. A return of premium rider refunds a portion of the premiums paid if you do not file a claim during a specified period. This rider can help offset the cost of disability insurance if you remain healthy and do not need to use the benefits. The return of premium rider usually refunds a percentage of the total premiums paid, often 50% to 80%, after a predetermined period, such as 10 or 15 years. Some policies may also offer a full refund of premiums paid at the end of the policy term. The definition of disability in your policy determines the circumstances under which you are eligible for benefits. An "own occupation" means you are considered disabled if you cannot perform the duties of your specific occupation, while an "any occupation" definition requires that you are unable to perform the duties of any occupation for which you are reasonably suited by education, training, or experience. Some policies differentiate between partial and total disability, with different benefits or coverage periods for each. Partial disability usually refers to a situation where you can still work, but with reduced hours or responsibilities, while total disability means you cannot work at all. The benefit period is the length of time for which you will receive disability benefits. Benefit periods can range from a few months to several years, or even up to retirement age. A longer benefit period generally results in higher premium costs. The longer the benefit period, the higher the premium costs. It is essential to consider the potential duration of a disability when selecting a benefit period, as well as the impact on your budget and financial planning. The elimination period, also known as the waiting period, is the duration you must be disabled before your benefits begin. Elimination periods can range from a few days to several months, with longer waiting periods resulting in lower premium costs. A longer elimination period generally results in lower premium costs. However, it also means you will have to wait longer before receiving benefits, so it is crucial to consider your financial situation and ability to cover expenses during this waiting period. A non-cancelable policy guarantees that your insurer cannot cancel your policy or increase your premiums as long as you continue to pay the premiums. A guaranteed renewable policy also ensures that the insurer cannot cancel your policy, but they may increase your premiums based on factors such as age or changes in the risk pool. Both non-cancelable and guaranteed renewable policies provide a level of protection for policyholders, ensuring that their coverage remains in place. However, non-cancelable policies offer more premium stability and predictability, while guaranteed renewable policies may be subject to premium increases. To choose the right riders and policy features, it is crucial to evaluate your personal needs, potential risks, and financial situation. Factors to consider include your occupation, income, health, and family circumstances. When selecting riders and policy features, it is essential to weigh the potential benefits against the additional costs. Carefully consider whether each rider or feature offers sufficient value to justify the added expense. A financial advisor or insurance agent can provide valuable guidance in selecting the appropriate riders and policy features for your specific needs. They can help you understand the options available and make informed decisions based on your personal circumstances. Disability insurance is a critical component of financial planning that offers protection against the loss of income due to illness or injury. Selecting the right riders and policy features is essential to create a tailored plan that meets your unique needs and circumstances. By carefully considering the various riders and policy features available, you can find the right balance between cost and coverage, ensuring adequate protection for your financial well-being. Consulting with a financial advisor or insurance agent can further help you make informed decisions about the most appropriate riders and policy features for your situation. Ultimately, investing time and effort into understanding and customizing your disability insurance policy is a crucial step in securing your financial future and safeguarding your income in the face of potential disability.Disability Insurance: Overview

Short-Term Disability Insurance

Long-Term Disability Insurance

Social Security Disability Insurance

Business Overhead Expense Insurance

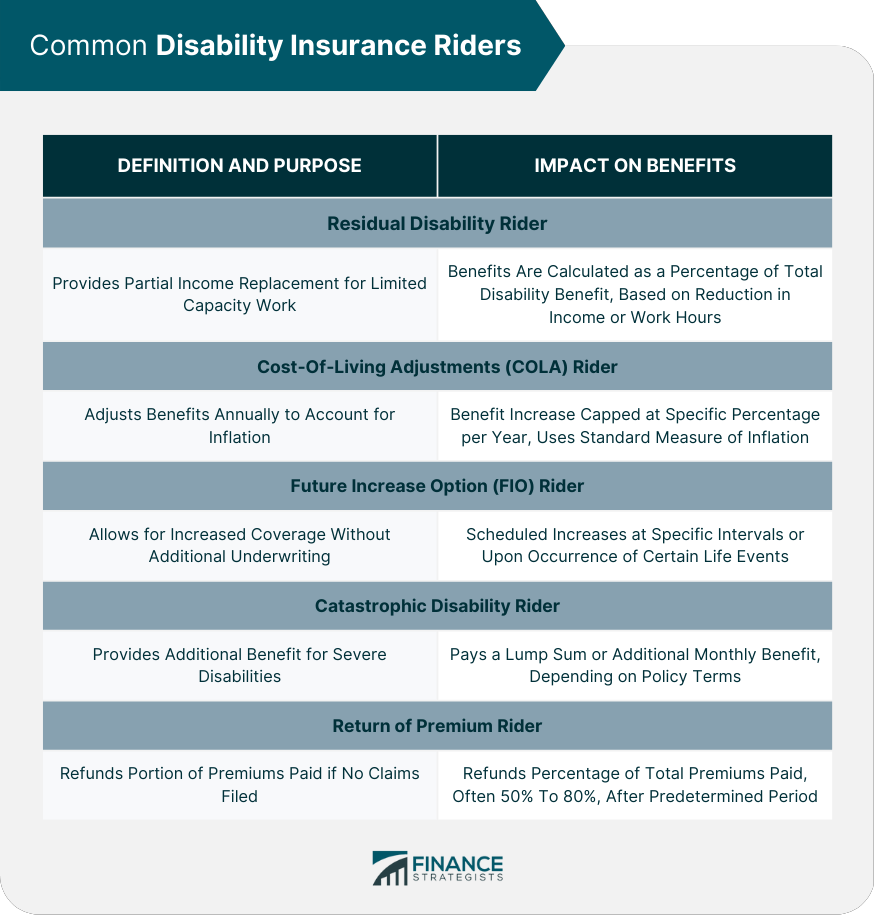

Common Disability Insurance Riders

Residual Disability Rider

Definition and Purpose

Calculation of Benefits

Cost-Of-Living Adjustments (COLA) Rider

Definition and Purpose

Impact on Benefits

Future Increase Option (FIO) Rider

Definition and Purpose

Increase in Coverage Without Additional Underwriting

Catastrophic Disability Rider

Definition and Purpose

Benefits During Severe Disabilities

Return of Premium Rider

Definition and Purpose

Refund of Premiums Paid

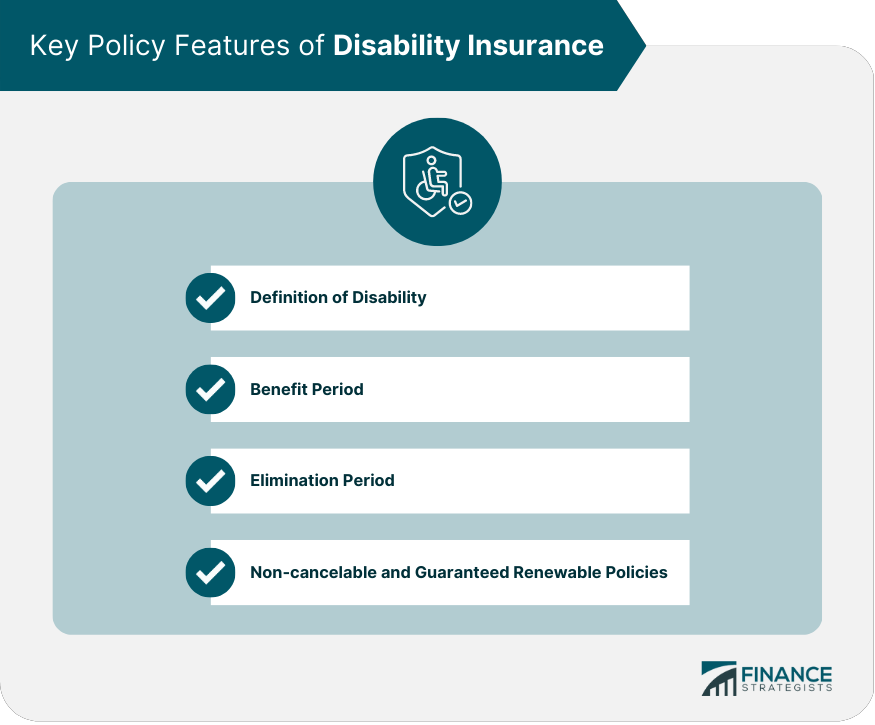

Key Policy Features of Disability Insurance

Definition of Disability

Own Occupation vs Any Occupation

Partial vs Total Disability

Benefit Period

Duration of Benefits

Impact on Premium Costs

Elimination Period

Waiting Period Before Benefits Start

Impact on Premium Costs

Non-cancelable and Guaranteed Renewable Policies

Definitions and Differences

Impact on Policyholder's Rights and Premium Stability

Choosing the Right Riders and Policy Features

Assessing Personal Needs and Risks

Evaluating the Cost-Benefit Ratio

Consulting With a Financial Advisor or Insurance Agent

Conclusion

Disability Insurance Riders and Policy Features FAQs

A disability insurance rider is an optional add-on to a disability insurance policy that provides additional coverage for specific risks or circumstances. Some common riders include cost-of-living adjustments, residual disability benefits, and future insurability options.

A cost-of-living adjustment rider, also known as a COLA rider, is a rider that increases your disability insurance benefits over time to keep pace with inflation. This helps ensure that your benefits maintain their purchasing power in the event of a long-term disability.

A residual disability benefit rider is a rider that provides partial disability benefits if you are able to work but have a reduction in income due to your disability. This rider can help make up for lost income and bridge the gap until you are able to return to work full-time.

A future insurability option rider is a rider that allows you to increase your disability insurance coverage in the future without having to undergo additional medical underwriting. This rider can be helpful if your income increases over time and you need more coverage to adequately protect yourself and your family.

A non-cancelable and guaranteed renewable policy feature is a policy feature that guarantees that your policy cannot be canceled by the insurer as long as you continue to pay your premiums on time. Additionally, your premiums cannot be increased by the insurer unless they are increased for all policyholders in the same class. This provides you with long-term stability and certainty in your disability insurance coverage.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.