Disability Buy-Out Insurance is a type of insurance policy that provides protection to business owners in the event that one of the owners becomes disabled and is no longer able to work. The policy pays out a lump sum of money to the remaining owners, allowing them to buy out the disabled owner's share of the business. This type of insurance is important for any business that has multiple owners, as it provides financial protection and ensures that the business can continue to operate in the event of a disability. Disability Buy-Out Insurance is typically structured as a disability policy that is owned by the business, rather than by the individual owners. If a covered owner becomes disabled and is unable to work for a specified period of time, typically 12-24 months, the policy pays out a lump sum of money to the remaining owners. This money can be used to buy out the disabled owner's share of the business, allowing the remaining owners to continue running the business without interruption. A disability buy-out policy typically includes several key components that define the terms of the coverage: Definition of Disability: The policy will have a specific definition of disability, which determines when benefits will be paid out. This can include total disability or partial disability, depending on the policy. Waiting Period: This is the period of time that must pass after the onset of the disability before benefits are paid out. Waiting periods can range from a few months to several years. Benefit Amount: The amount of money that will be paid out to buy out the disabled owner's share of the business. This is typically determined based on a valuation of the business. Buy-Out Structure: The policy will outline how the buy-out of the disabled owner's share will be structured, such as through an entity purchase agreement or a cross-purchase agreement. Premiums: The cost of the policy, which will depend on factors such as the age, health, and occupation of the insured owners, as well as the size and type of business. There are two main types of disability buy-out insurance: Entity Purchase Agreement: This type of agreement involves the business itself purchasing a policy on each of the owners. In the event of a disability, the business will receive the payout and use it to buy out the disabled owner's share. Cross-Purchase Agreement: In this arrangement, each business owner individually purchases a policy on the other owners. If one owner becomes disabled, the other owners receive the payout and use it to buy out the disabled owner's share. To be eligible for disability buy-out insurance, a business typically needs to meet certain underwriting requirements, such as having a formal buy-sell agreement in place and providing financial information about the company. The underwriting process may also include medical exams for the insured owners. Disability buy-out insurance can help ensure the continuity and stability of the business by: Ensuring Business Continuity: The policy provides the necessary funds to buy out the disabled owner's share, allowing the business to continue operating without interruption. Maintaining the Value of the Company: By facilitating a smooth transition of ownership, disability buy-out insurance helps preserve the value of the business and prevents a fire sale situation. A disability buy-out policy provides financial security for the disabled owner by: Providing Financial Security: The disabled owner receives a fair value for their share of the business, ensuring they have the financial resources they need during a challenging time. Facilitating a Smooth Exit from the Business: The policy allows the disabled owner to exit the business without causing disruption, making it easier for them to focus on their recovery. Disability buy-out insurance also benefits the remaining business owners and stakeholders by: Preventing Unwanted Ownership Changes: The policy ensures that ownership stays within the intended group of owners, preventing outsiders from acquiring a stake in the business. Maintaining Company Stability: By providing the funds needed to buy out the disabled owner's share, the policy helps maintain the stability of the company, reassuring employees, customers, and suppliers. Disability buy-out insurance is just one of several insurance products that can help protect businesses and their owners. It is essential to understand how it compares to these other products: Disability Income Insurance: This type of insurance provides a monthly income to the insured individual if they become disabled and cannot work. While it helps cover personal expenses, it does not address the needs of the business. Key Person Insurance: This policy covers the loss of a key employee due to death or disability. The payout is made to the business to help cover financial losses and find a replacement, but it does not provide funds for a buy-out of the disabled owner's share. Business Overhead Expense Insurance: This insurance covers ongoing business expenses, such as rent and payroll, if the owner becomes disabled. While it helps keep the business running, it does not address ownership issues. Life Insurance: Life insurance provides a payout upon the death of the insured individual. While it can be used in conjunction with a buy-sell agreement to address the death of an owner, it does not cover disability. To choose the right disability buy-out insurance policy, it is essential to carefully assess the needs of the business and its owners. This includes considering factors such as the size of the business, the number of owners, and the potential financial impact of a disability on the company. There are numerous insurance providers that offer disability buy-out insurance policies. It is crucial to research and compare different providers to find the one that offers the best coverage, pricing, and customer service. Before purchasing a policy, it is essential to carefully review and understand the terms and conditions, including the definition of disability, waiting periods, benefit amounts, and buy-out structures. This will help ensure that the policy meets the needs of the business and its owners. An insurance broker or advisor can provide valuable guidance when selecting a disability buy-out insurance policy. They can help evaluate different providers, navigate the underwriting process, and ensure that the chosen policy is the best fit for the business and its owners. Disability buy-out insurance plays a critical role in safeguarding the financial stability and continuity of a business in the event of an owner's disability. By understanding the key components of a disability buy-out policy, such as the definition of disability, waiting period, benefit amount, buy-out structure, and premiums, business owners can better assess their needs and choose the right coverage. Additionally, evaluating different types of disability buy-out insurance, such as entity purchase agreements and cross-purchase agreements, helps ensure the most suitable arrangement for the business. It is essential to recognize the benefits of disability buy-out insurance, including the protection it offers to the business, disabled owner, and other owners and stakeholders. By comparing disability buy-out insurance with other insurance products, such as disability income insurance, key person insurance, business overhead expense insurance, and life insurance, business owners can make informed decisions about their overall insurance strategy. Lastly, by working with an insurance broker or advisor, business owners can evaluate different providers, navigate the underwriting process, and ensure the chosen policy is the best fit for the business and its owners.What Is Disability Buy-Out Insurance?

Understanding Disability Buy-Out Insurance

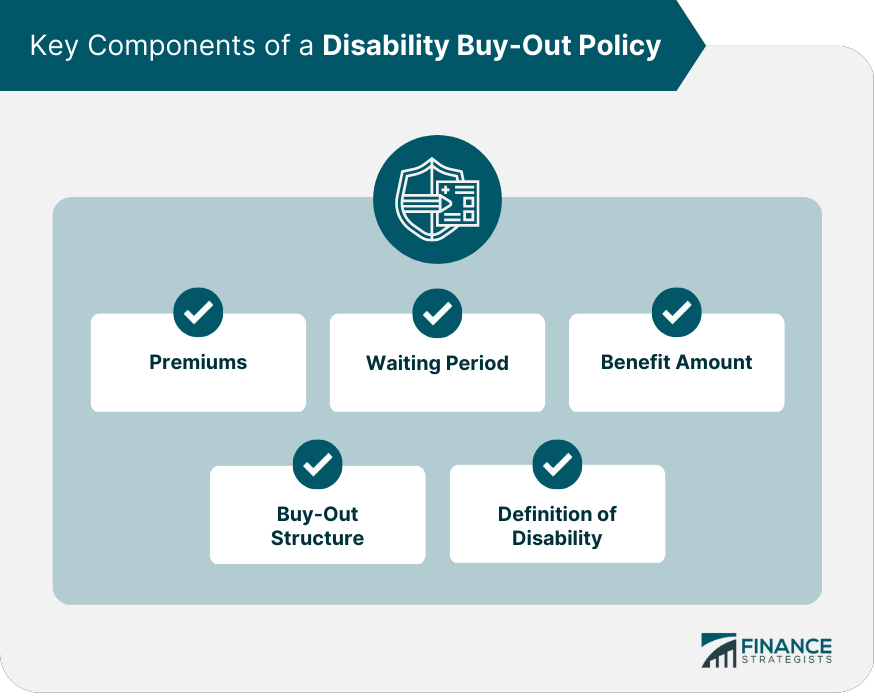

Key Components of a Disability Buy-Out Policy

Types of Disability Buy-Out Insurance

Eligibility and Underwriting Requirements

Benefits of Disability Buy-Out Insurance

Protection of the Business

Protection of the Disabled Owner

Protection of Other Owners and Stakeholders

Comparing Disability Buy-Out Insurance With Other Insurance Products

Choosing the Right Disability Buy-Out Insurance Policy

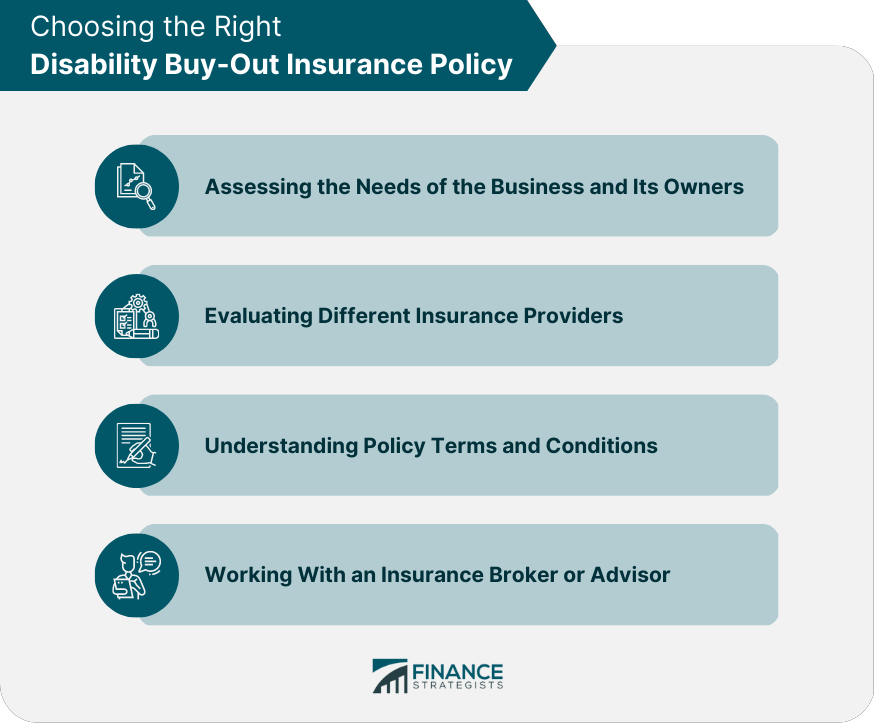

Assessing the Needs of the Business and Its Owners

Evaluating Different Insurance Providers

Understanding Policy Terms and Conditions

Working With an Insurance Broker or Advisor

Conclusion

Disability Buy-Out Insurance FAQs

Disability Buy-Out Insurance is a type of insurance policy that provides protection to business owners in the event that one of the owners becomes disabled and is no longer able to work. The policy pays out a lump sum of money to the remaining owners, allowing them to buy out the disabled owner's share of the business.

Disability Buy-Out Insurance is important for any business that has multiple owners. If one of the owners becomes disabled and can no longer contribute to the business, it can be difficult for the remaining owners to continue running the business without their input. Disability Buy-Out Insurance provides financial protection and ensures that the business can continue to operate.

The amount of Disability Buy-Out Insurance you need will depend on the value of your business and the percentage of ownership each owner holds. It is important to work with an experienced insurance professional who can help you determine the appropriate amount of coverage needed.

The cost of Disability Buy-Out Insurance varies depending on a number of factors, including the size and type of business, the age and health of the owners, and the amount of coverage needed. It is important to shop around and compare quotes from multiple insurance providers to find the best coverage at the most affordable price.

Yes, Disability Buy-Out Insurance can be customized to meet the specific needs of your business. You can choose the amount of coverage, the length of the waiting period before benefits are paid, and the length of time benefits will be paid out. Working with an experienced insurance professional can help ensure that your policy is tailored to meet your unique needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.