Interest income planning is a financial strategy that focuses on maximizing the interest earned on your investments while minimizing taxes and risks. It involves carefully choosing investment options, such as bonds, CDs, and money market funds, based on their interest rates and other factors. The goal of interest income planning is to generate a steady stream of income from your investments without taking on excessive risks. Interest income planning may involve considering factors such as the expected duration of your investment, the tax implications of different investment options, inflation rates, and market conditions. By optimizing your investments for interest income, you can increase your returns and make your money work harder for you. Interest income planning is particularly relevant for individuals who are retired or nearing retirement, as they often rely on interest income from their investments to fund their living expenses. However, it can be beneficial for anyone who is looking for a way to generate passive income from their savings and investments. Savings accounts are among the simplest and most accessible sources of interest income. They provide a low-risk and highly liquid investment, making them ideal for emergency funds and short-term savings. CDs are time-bound deposit accounts offered by banks, requiring investors to commit their funds for a specified term. In return, they offer a higher interest rate than traditional savings accounts. CDs are considered low-risk investments and are often used for short-to-medium-term savings. Bonds are fixed-income securities issued by governments, municipalities, and corporations to raise capital. They pay periodic interest, known as coupon payments, and return the principal upon maturity. Government bonds are issued by national governments and are generally considered to be among the safest investments. They can be short-term (Treasury bills), medium-term (Treasury notes), or long-term (Treasury bonds) investments. Municipal bonds are issued by local governments or government agencies to fund public projects. They are generally considered low-risk investments and may offer tax advantages, as interest income is often exempt from federal and, in some cases, state and local taxes. Corporate bonds are issued by companies to raise capital for business operations or expansion. They typically offer higher interest rates than government bonds, reflecting the increased risk associated with investing in individual companies. Fixed-income mutual funds pool investors' money to purchase a diversified portfolio of bonds and other fixed-income securities. They offer professional management, diversification, and liquidity, making them an attractive option for investors seeking interest income. Peer-to-peer (P2P) lending platforms connect individual borrowers with investors, allowing investors to earn interest income by lending money directly to borrowers. P2P lending typically offers higher interest rates than traditional fixed-income investments but comes with increased risk. Annuities are long-term investment products issued by insurance companies that provide a guaranteed stream of income, either immediately or in the future. They can be an effective tool for generating interest income during retirement. Although not fixed-income investments, dividend-paying stocks can provide regular income in the form of dividends. Investors seeking interest income may consider allocating a portion of their portfolio to these stocks as part of a diversified income strategy. Diversification involves spreading investments across multiple asset classes and sectors to minimize risk. By investing in a mix of fixed-income securities, investors can reduce the impact of poor performance in any single investment. Laddering is a strategy that involves investing in a series of bonds or CDs with staggered maturity dates. This approach provides regular cash flow, reduces interest rate risk, and allows for reinvestment at potentially higher rates. Investors should consider the tax implications of their interest income investments and seek tax-efficient options, such as municipal bonds or tax-deferred accounts, to minimize their tax burden. Risk management involves evaluating the creditworthiness of bond issuers, considering interest rate risk, and maintaining an appropriate level of diversification to protect against market fluctuations. Reinvesting interest income can help grow your investment portfolio over time and take advantage of compounding returns. Investors can choose to automatically reinvest interest income into the same investment or allocate it to other investments to maintain their desired asset allocation. Asset allocation is the process of dividing your investments among different asset classes, such as stocks, bonds, and cash, based on your risk tolerance, investment goals, and time horizon. Regularly reviewing and adjusting your asset allocation can help ensure that your interest income plan stays aligned with your financial objectives. Your investment time horizon, or the period you expect to hold your investments before needing the funds, plays a critical role in interest income planning. Investors with a longer time horizon can afford to take on more risk and allocate a larger portion of their portfolio to higher-yielding investments. Interest income can be either taxable or tax-exempt, depending on the type of investment. Taxable interest income is subject to federal, state, and local taxes, while tax-exempt interest income, such as that from certain municipal bonds, is not subject to federal taxes and may be exempt from state and local taxes as well. Investors should be aware of the various tax rates that apply to their interest income, as these rates can significantly impact their after-tax returns. It is essential to consider federal, state, and local tax rates when making investment decisions and planning for taxes. There are several tax planning strategies that can help investors minimize their tax burden and maximize their after-tax returns: Tax-Deferred Accounts: Tax-deferred accounts, such as individual retirement accounts (IRAs) and 401(k) plans, allow investors to postpone paying taxes on interest income until they withdraw the funds, typically during retirement. Tax-Free Municipal Bonds: Investing in tax-free municipal bonds can help reduce your tax burden, as interest income from these bonds is generally exempt from federal taxes and, in some cases, state and local taxes. Tax-Efficient Fund Placement: Placing investments with higher tax implications, such as taxable bonds, in tax-deferred accounts, and investments with lower tax implications, such as municipal bonds, in taxable accounts can help optimize after-tax returns. Investors with tax-deferred retirement accounts must begin taking required minimum distributions (RMDs) once they reach a certain age, typically 72. RMDs are subject to income taxes, so investors should plan for these withdrawals and their tax implications. Investors should regularly review their interest income plan to ensure it remains aligned with their financial goals, risk tolerance, and market conditions. This may involve updating the plan to reflect changes in personal circumstances, such as a new job or the birth of a child. Interest income planning should be responsive to changes in market and economic conditions. Investors may need to adjust their plans to account for fluctuations in interest rates, inflation, and other economic indicators. As life circumstances change, so too may your financial goals. Revisiting your interest income plan and adjusting it accordingly can help ensure that your investments continue to support your evolving needs. Periodically evaluating the performance of your interest income investments can help you identify underperforming assets and opportunities for improvement. Comparing your investments' performance to relevant benchmarks can provide valuable insights into your plan's effectiveness. Rebalancing involves adjusting your asset allocation to maintain your desired level of risk and return. Regular rebalancing can help ensure that your interest income plan remains in line with your investment goals and risk tolerance, particularly as market conditions change or as your investments grow over time. Working with a financial advisor can provide valuable guidance and expertise in developing and managing your interest income plan. Advisors can help you assess your risk tolerance, set realistic financial goals, and recommend appropriate investment strategies tailored to your unique needs. Selecting the right financial advisor is crucial for ensuring a successful partnership. Factors to consider when choosing an advisor include their qualifications, experience, communication style, and compatibility with your financial goals and needs. Financial advisors may charge fees based on assets under management (AUM), hourly rates, or flat fees for specific services. Understanding an advisor's fee structure and associated costs can help you make an informed decision when selecting a professional to assist with your interest income planning. A long-term relationship with a financial advisor can provide ongoing support, guidance, and expertise as your financial goals and circumstances evolve over time. Regular communication and updates can help ensure that your interest income plan remains aligned with your changing needs and objectives. Effective interest income planning is essential for maximizing returns, minimizing risk, and achieving long-term financial goals. By understanding the various sources of interest income, implementing sound planning strategies, considering tax implications, and working with a trusted financial advisor, investors can create a well-rounded interest income plan that supports their financial success.What Is Interest Income Planning?

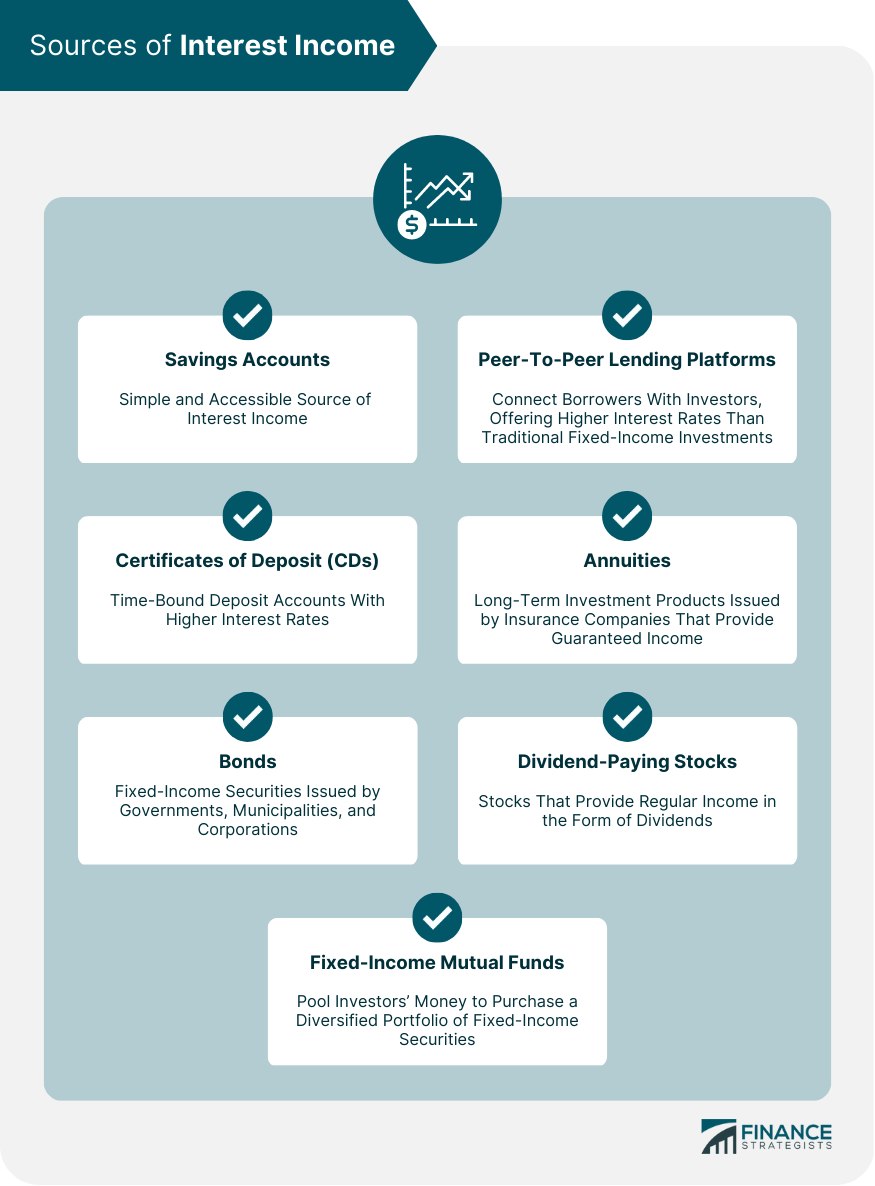

Sources of Interest Income

Savings Accounts

Certificates of Deposit (CDs)

Bonds

Government Bonds

Municipal Bonds

Corporate Bonds

Fixed-Income Mutual Funds

Peer-To-Peer Lending Platforms

Annuities

Dividend-Paying Stocks

Interest Income Planning Strategies

Diversification

Laddering

Tax-Efficient Investments

Risk Management

Reinvesting Interest Income

Asset Allocation

Time Horizon Considerations

Tax Implications and Considerations

Taxable vs Tax-Exempt Interest Income

Federal, State, and Local Taxes

Tax Planning Strategies

Required Minimum Distributions (RMDs)

Monitoring and Adjusting Your Interest Income Plan

Regular Reviews and Updates

Market and Economic Changes

Changes in Personal Financial Goals

Performance Evaluation

Rebalancing

Working With a Financial Advisor

Benefits of Professional Advice

Choosing the Right Advisor

Fee Structures and Costs

Establishing a Long-Term Relationship

Conclusion

Interest Income Planning FAQs

Interest income planning is a financial strategy to maximize the interest earned on your investments while minimizing taxes and risks. It involves careful consideration of different investment options, such as bonds, CDs, and money market funds, as well as tax implications, inflation, and market conditions.

Interest income planning is important because it can help you generate a steady stream of income without taking on excessive risks. By optimizing your investments for interest income, you can increase your returns and make your money work harder for you.

Some common strategies for interest income planning include diversifying your portfolio across different types of investments, such as short-term and long-term bonds, and adjusting your holdings based on changing market conditions. You may also consider investing in tax-deferred accounts, such as IRAs or 401(k)s, to minimize taxes on your interest income.

The main risks associated with interest income planning are interest rate risk, credit risk, and inflation risk. Interest rate risk refers to the potential for interest rates to rise, which can cause the value of your investments to decline. Credit risk refers to the risk of default by the issuer of your bonds or other fixed-income securities. Inflation risk refers to the risk that rising prices will erode the purchasing power of your interest income over time.

To get started with interest income planning, it's important to assess your financial goals, risk tolerance, and investment horizon. You may want to consult with a financial advisor or use online tools to help you identify suitable investments and develop a customized strategy. It's also important to monitor your investments regularly and adjust your strategy as needed based on market conditions and your changing needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.