Capital expenditures or capital expenses are funds used by companies or businesses for the purchase, improvement, and maintenance of long-term assets. These long-term assets must have a useful life of a year or more and are intended to enhance the efficiency of a business. They are usually physical, fixed, and non-consumable assets such as property, equipment, or infrastructure. However, they can also include intangible assets such as a patent or license. Capital expenditures are recorded on cash flow statements under investing activities and on the balance sheet, usually under property, plant, and equipment (PP&E). Unlike operating expenses (OpEx), capital expenditures are not recorded in full during the period in which they were incurred. Instead, they are deducted over time as a depreciation expense, starting the year after the item was obtained. There are three types of business expenses recognized by the Internal Revenue Service (IRS) as capital expenditures. They are the following: Business startup costs are the initial funds spent on getting a business up and running. For example, when a small company is looking to start a new business in a new city it may spend money on market research, feasibility studies, or environmental impact assessments. Some business startup costs can be considered capital expenditures while others are counted as operating expenses. Startup costs are categorized into capital expenditures or operating expenses, depending on how long it takes to recover each specific cost through future revenues. Costs that are related to future revenues, such as buildings, patents, or machines, are typically considered capital expenditures. Meanwhile, costs that are not related to generating future revenues, such as rent, advertising, or salaries, are considered operating expenses. These are capital expenses made to acquire long-term assets that will be used in business operations. This may include land, buildings, vehicles, furniture, office equipment, machinery, and franchise rights. For instance, a company may purchase a fleet of vehicles to deliver its products. The cost of the vehicles would be considered a capital expenditure since it is a long-term asset that will be used to generate income for the company. Improvements are capital expenses incurred to increase the value or prolong the useful life of long-term assets. This may include activities such as replacing a major part of some equipment or making additions to an existing property. For example, a company decides to renovate its office space so that it can be used by a new division. In this case, the renovation cost would be considered a capital expenditure, since it will increase the value of the office space and prolong its useful life. The formula for calculating capital expenditures is as follows: The formula above mentions Property, Plant, and Equipment.. These are fixed, tangible assets utilized by businesses to generate revenue and profit. These typically include machinery, buildings, vehicles and land. When a company uses funds to purchase these items, they are recorded as part of the total PP&E on the balance sheet. Depending on the nature of the business, most capital expenditures fall under the category of Property, Plant, and Equipment while some do not. For instance, patents and licenses are intangible assets and thus not included in the PP&E category. Instead, they may have their own separate category in the balance sheet. In cases like these, we can revise our formula to take into account the value of both the PP&E and the other intangible capital expenditures. Capital expenditures are not deducted as an expense on the month in which they were incurred, instead, they are amortized or depreciated over the span of their useful life. PP&E items are depreciated while intangible assets such as patents or licenses are amortized. Depreciation is the periodical allocation of a tangible asset’s cost on the balance sheet. Amortization functions in the same way, but is more focused on intangible assets. Depreciation and amortization are done because the value of most capital expenditures decreases over time, mostly through wear and tear. In the formula above, depreciation is considered a factor in computing capital expenditures. In cases where a company has purchased intangible assets as part of its capital expenditures, the formula may be modified to include both depreciation and amortization. To illustrate, let us determine the capital expenditure of XYZ corporation in 2021 using the information presented below: Taking the highlighted figures from the information above, the calculation would be: CapEx = Current PP&E – Prior PP&E + Current Depreciation =74,550.00 - 72,300.00 + 10,000.00 = $12,250.00 The resulting CapEx figure shows that in 2021, XYZ Corporation invested $12,250.00 in property, plant, and equipment. The cash flow to capital expenditures ratio measures the ability of a company to purchase capital assets using the cash generated from its operations. A high ratio reveals that a company has a lesser need to utilize debt or equity funding since it has enough cash to cover possible capital expenditures. In contrast, a low ratio shows that a company may not have enough funds available to make capital purchases. In cases like these, it may choose to take out a loan or postpone necessary expenses due to the lack of funding. The cash flow to capital expenditures ratio is calculated by dividing the cash flow from operations by its capital expenditures. The formula is as follows: For example, let us say that a company has $200,000 in its cash flow from operations and spends $100,000 on capital expenditures. The cash flow to capital expenditures ratio would be 2. Cash Flow to Capital Expenditures = $200,000 / $100,000 = 2 This indicates that for every $2 dollars of cash gained through its business operations, the company has previously allotted around $1 dollar for capital expenditures. Based on this result, the company may choose to either increase or decrease the amount they spend on capital expenditures. Regardless of which direction it chooses to go in, the company has more than enough cash from its business operations to fund any possible capital expenses, without raising capital through loans or selling of shares. Capital expenditures play a key role in the growth and expansion of businesses. By reinvesting funds back into the business, companies are able to acquire new assets, improve existing ones, and expand their operations. However, the decision to start a project involving much capital expenditure must be carefully analyzed as it will have a significant impact on the financial position and cash flow of a company. Below are a few other reasons why companies need to deliberate before deciding how much to spend on capital expenditure: Capital expenditures are mostly considered irreversible decisions because they involve a long-term commitment of resources. Most assets acquired under capital expenditure cannot be easily reversed without incurring some loss for the business. For example, after a company acquires a piece of equipment, it may be difficult to resell it at its original price. This is because it would now be considered used equipment, which is less attractive to buyers than newer models. In other words, capital expenditures are considered sunk costs, and businesses have to "sink or swim" with their decisions. Capital expenditures typically involve high initial costs. For example, constructing a new building would require a large amount of upfront capital which may strain the company's financial resources. When assets are put into use, they will gradually lose their value over time due to wear and tear, obsolescence, or changes in market conditions. This is why it is very critical to evaluate during the initial stages whether an expenditure is justified. For example, a company must weigh the pros and cons of investing in a new computer system that will have a useful life of five years. The company must determine if the benefits of the new system would outweigh its costs after taking into account factors such as depreciation. Capital expenditure decisions can have life-long effects on businesses. Once a decision is made, it is very difficult and costly to change course. For instance, if a company decides to build a new factory in a certain location, it would be very difficult and expensive to move the factory to another location if the original decision turns out to be wrong. This is why it is very important for companies to carefully consider all options before making a capital expenditure decision. Despite the many benefits associated with capital expenditures, there are also some challenges that come along with it. These include: It is not guaranteed that a company will achieve the expected results from its capital expenditures. This is due to several factors that can affect the outcome of a project, such as economic conditions, changes in technology, and competition. For example, a company may build a new factory expecting to increase production by 30%. However, if the economy weakens or competition intensifies, the company may only see a 20% increase in production. This is why it is important for companies to have a contingency plan in place in case the expected results are not achieved. Measuring and estimating the costs and benefits of capital expenditures can be a complex and challenging task. For instance, it may be difficult to determine how much revenue a new factory will generate or how much cost savings will be achieved from a new computer system. There are also intangible results of capital expenditures that are difficult to measure, such as the impact on employee morale or the company's reputation. The costs and benefits of capital expenditures are often spread out over a long period of time. This makes it more difficult to determine the true financial impact of a project. For example, the full benefits of a new machine may not be realized for several years after it is purchased. This makes it difficult to estimate the discount rate and establish equivalence. Budgeting for capital expenditures must be carefully planned and executed. Here are some of the best practices to ensure more efficient capital expenditure budgeting: The first step in efficient capital expenditure budgeting is to have a clear and concise plan. The plan should include the company's goals and objectives, as well as the projects that will be undertaken to achieve these goals. Project scope and details should be clearly defined. The plan should also include strategies to mitigate any risks associated with upcoming projects. Department heads are well aware of the needs of their respective departments. Thus, they should be given the opportunity to provide input on capital expenditure budgeting. A bottom-up approach ensures that all relevant departments have a voice in the budgeting process, which increases the chances of a company's capital resources being used efficiently. It is important to have separate budgets for capital expenditures and operational expenses. Doing so will ensure that the company's capital resources are properly allocated and used for their intended purpose. It will also make it simpler to calculate the separate deductions involving each type of expense. This is because tax deductions on operational expenses apply to the current year, while deductions on capital expenditures can be spread out over a period of time through depreciation or amortization. It is important to set a budget limit for capital expenditures. This will help ensure that a business does not overspend on projects and put itself at financial risk. Capital expenditure budgeting should be based on clear and concise policies. These policies should be designed to achieve the goals and objectives of the company. They must also be reviewed and updated on a regular basis to ensure that they are still relevant and effective. Capital expenditures should be measured and monitored to ensure they achieve the desired results. Some of the ways to do this include hurdle rates, return on investment ratios, and payback periods. Analyzing the results and returns from previous capital expenditures will also help companies make informed decisions about future projects. Once the strengths and weaknesses of previous projects are identified, steps can be taken to improve the efficiency of future projects. Capital expenditure budgeting is a critical task for any company. By following the best practices mentioned above, businesses can ensure that their capital resources are used efficiently and effectively. Some people confuse capital expenditures with operating expenses. Below is a comparison table highlighting the difference between the two:

Capital expenditures are defined as the costs of purchasing and upgrading fixed assets such as buildings, machinery, equipment, and vehicles. In contrast, operating expenses are the costs of supporting the current operations, such as wages, sales commissions, office rent, and advertising. Certain business startup costs, business assets, and improvements are the types of business expenses that can be considered capital expenditures. Capital expenditures are important for any company as they represent the investments made in the future of the business. Thus, it is important to follow best practices that ensure efficient capital expenditure budgeting. This includes formulating clear policies, measuring CapEx returns, and setting a budget limit. By following these best practices and understanding the difference between CapEx and OpEx, companies can ensure that their capital resources are used efficiently and effectively. What Are Capital Expenditures (CapEx)?

Types of Capital Expenditures

Business Startup Costs

Business Assets

Improvements

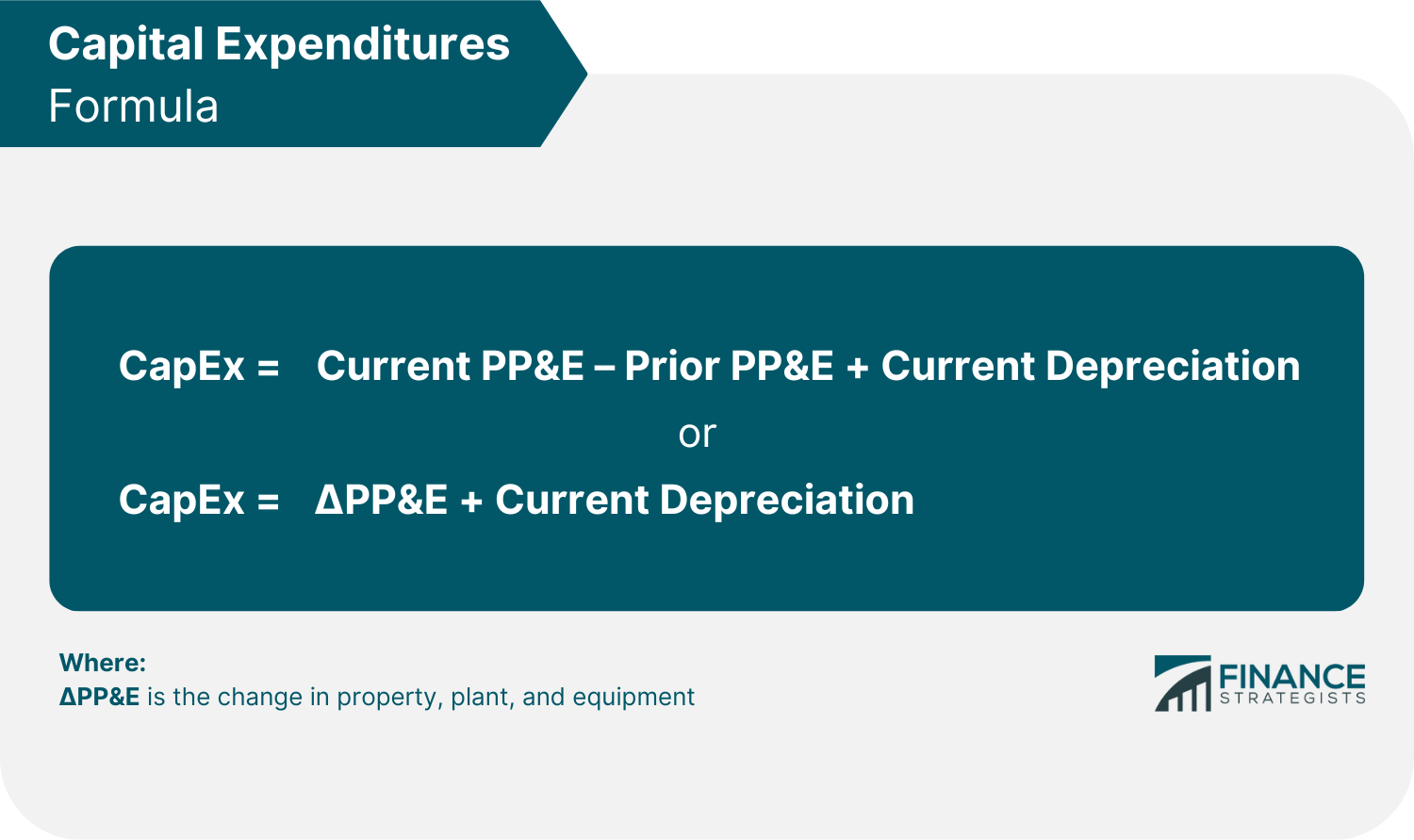

Formula for Capital Expenditures

Property, Plant and Equipment

Depreciation

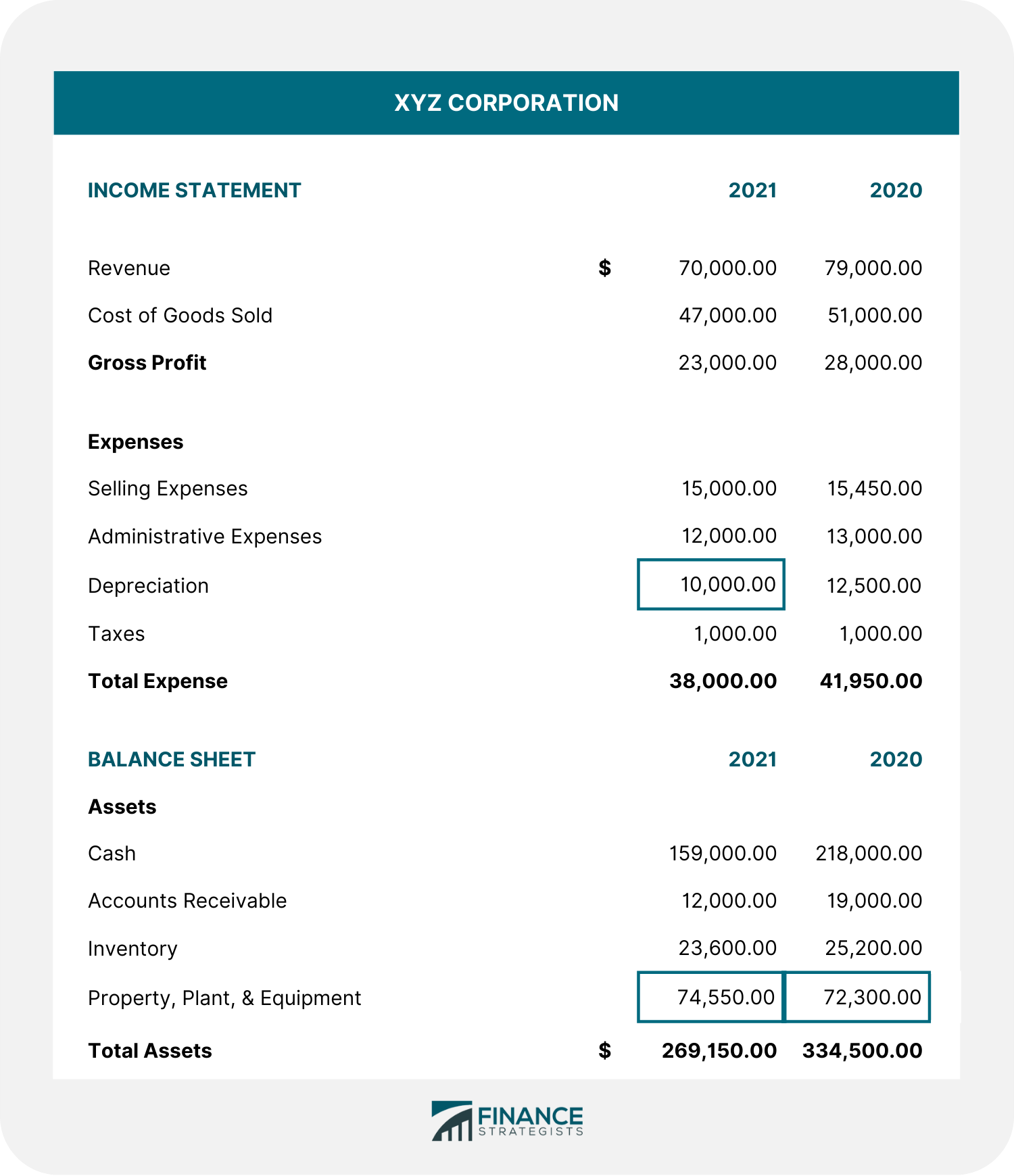

Sample Calculation of Capital Expenditures

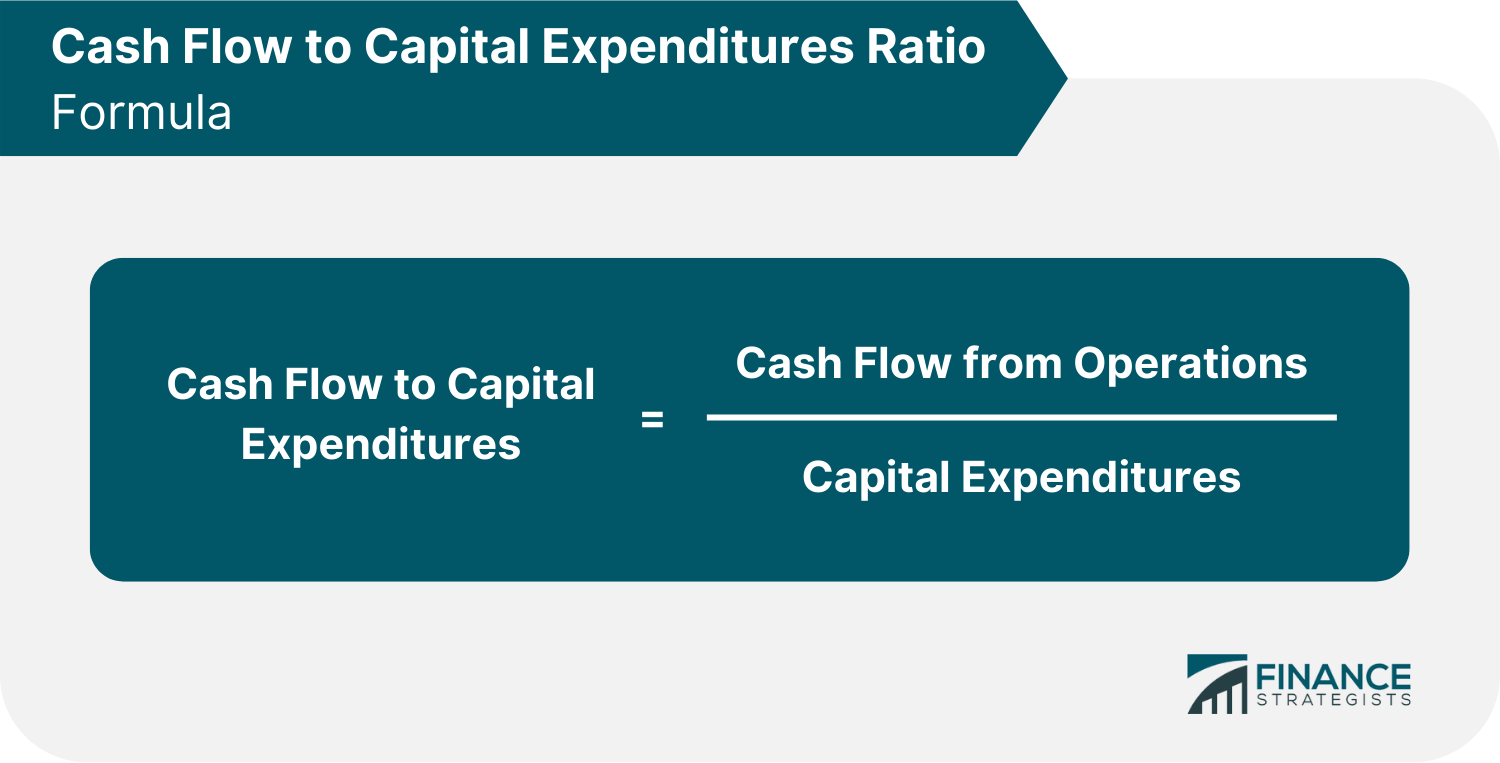

Cash Flow to Capital Expenditures Ratio

Importance of Capital Expenditure Decisions in Business

Irreversibility

Substantial Initial Costs

Depreciation

Long-Term Effects

Challenges of Capital Expenditures

Unpredictability in Forecasting

Measurement Difficulty

Temporal Spread

Best Practices for Efficient Capital Expenditure Budgeting

Sufficient Planning

Providing Inputs Through a Bottom-Up Approach

Separating Expenditure Budgets

Setting a Budget Limit

Forming Clear Policies

Measuring CapEx Returns

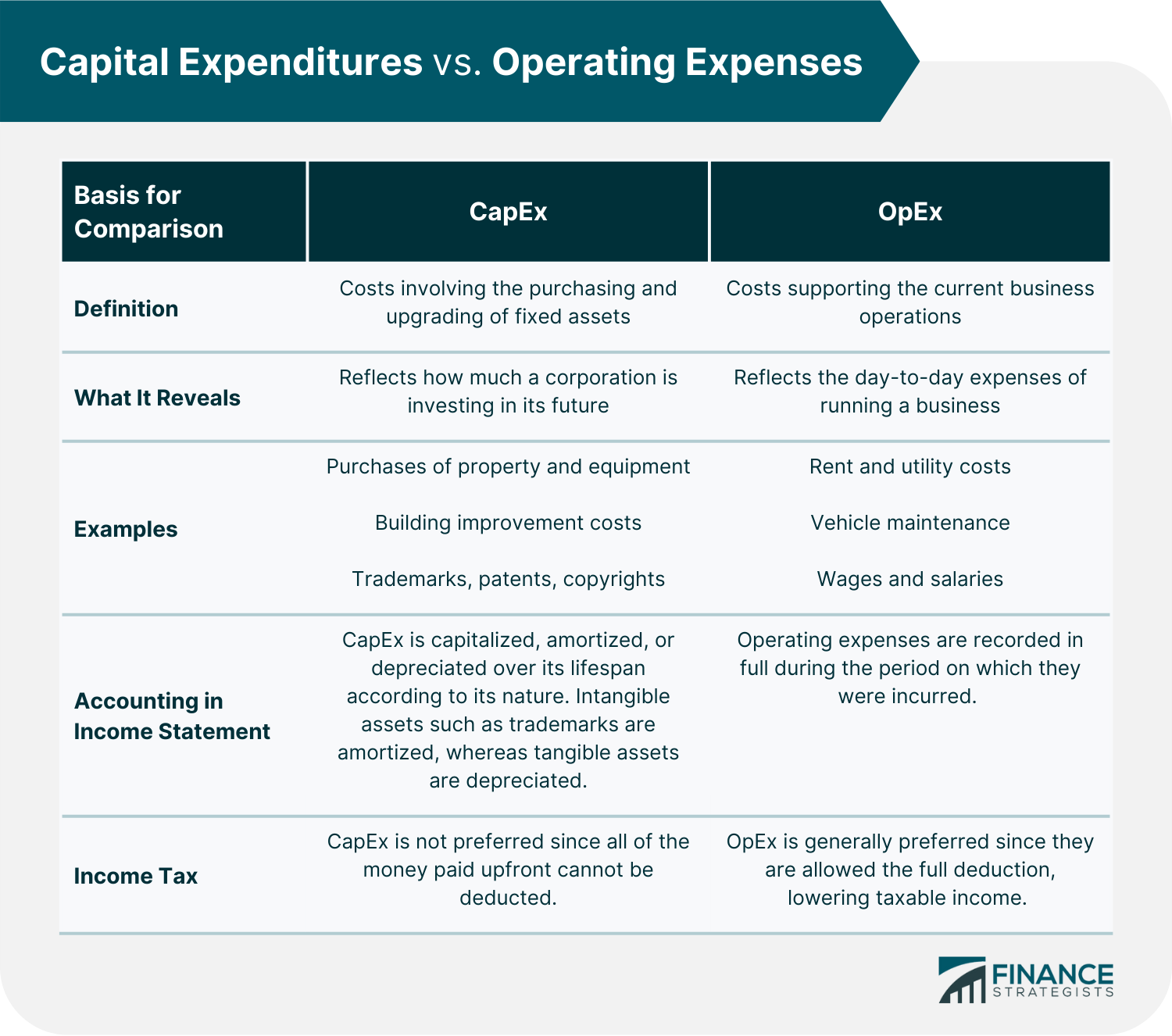

Capital Expenditures vs. Operating Expenses

The Bottom Line

Capital Expenditures FAQs

Capital expenditures are capitalized on the balance sheet as assets. They can also be reported as payments for property, plant, and equipment in a cash flow statement.

Capital expenditures are reported and classified as fixed assets. They are then charged as an expense over their useful life using depreciation or amortization.

Capital expenditures can be calculated using the following formulas: CapEx = Current PP&E – Prior PP&E + Current Depreciation or CapEx = Change in PP&E + Current Depreciation

Capital expenditures are the costs of purchasing and upgrading fixed assets such as buildings, machinery, equipment, and vehicles. In contrast, operating expenses are the costs of supporting the current operations, such as wages, sales commissions, office rent, and advertising.

No. Capital expenditures are not tax deductible. However, you can depreciate or amortize the cost of the asset over its useful life.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.